Producers and commodity marketing firms alike spend a good amount of time sifting through a never-ending firehose of data and information. The industry – including those of us at Total Farm Marketing – communicate a wide array of fundamental and technical factors we are tracking, and we use that data to help us make sense of the markets and to glean what may be developing. However, just because a development is interesting, it doesn’t necessarily mean that we should spend much (if any time) thinking about the impact on farm commodities. Our job is to filter out the noise and pay attention to what matters. Namely, what you get for your hard-earned production. We focus on information that is pertinent.

As a case in point, gold and silver have become one of the hottest commodity topics of late, and we’ve heard a lot about them in various publications and conversations. However – marketers need to ask: are gold and silver prices relevant (or not) to the decisions you make as a farm marketer?

The Allure of Silver and Gold

As you’ve undoubtedly heard, silver and gold have mounted one of the strongest rallies of the last 50 years. From October 2022 lows to the current levels in mid-February 2026, gold has rocketed upward at an annualized rate of roughly 45–50% and silver has exceeded gold at an annualized rate of roughly 60–70%.

To be sure, these recent returns don’t quite reach the levels triggered by the 2008 Global Financial Crisis, which triggered annualized returns of 70% for gold from 2008-2011 and ~150% for silver from 2009-2011. Quite notably, however, there is a case to be made that the current rallies reflect a structural upward shift in gold and silver pricing rather than a speculative bubble. Unlike the rallies 15 years ago and many like it, the current rallies are not a market reaction to an economic event, like a financial crisis or monetary easing.

Interesting, right? And there’s more. A commodity super cycle might be on deck.

A commodity super cycle is a long-duration (often 10-20+ year) period of structurally elevated demand across multiple commodity complexes that overwhelms supply capacity, driving sustained real price appreciation. Early signals tend to be driven by shifting strategic and global goals above and beyond a price objective, then followed by increases in demand for certain commodities.

The most recent commodity super cycle occurred as China exploded into the global markets from the 1990s through 2011, including the culmination in gold and silver prices that we discussed above. During that timeframe, gold typically posted its largest gains during periods of systemic stress.

The current gold rally fits a similar pattern. Sparked by the U.S. decision to freeze roughly $300 billion in Russian central bank assets after the 2022 invasion of Ukraine, global investors and sovereigns have increasingly sought to reduce reliance on the U.S. dollar. Gold—long regarded as a reliable store of value during crises and inflationary periods—has been the primary beneficiary.

Ag’s Potential in a Super Cycle

At this point, you may be thinking (as many producers have) that a commodity super cycle may well be poised to swell prices across commodities, including corn.

Great news, right?

Well, no. Unfortunately, as interesting as the increase in gold and silver and the potential for a super cycle are, it’s just noise when it comes to the corn pricing decisions you make. Based on data from Barchart, gold and corn futures have exhibited only a low positive correlation (generally below 15%) historically, which means that the rise and fall of gold (and silver) prices has almost no predictive value (either positive or negative) on the price of corn. While they may occasionally move in the same direction, their drivers are fundamentally different. Corn is governed by agricultural supply/demand and biofuel policy, while gold functions as a safe-haven and inflation hedge.

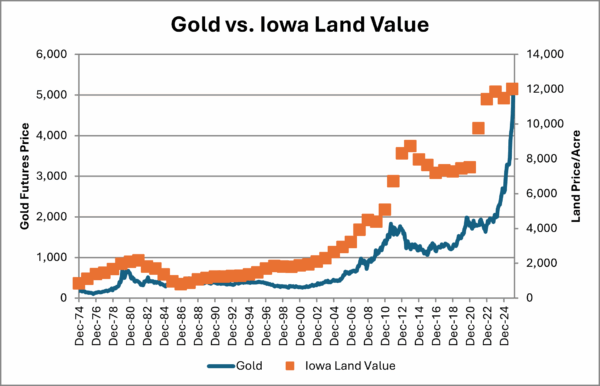

There is some correlation that may benefit you, but not with production. Take a look at the chart below which tracks gold and Iowa agricultural land prices (as a proxy for land prices overall) over the past 50 years. Gold and agriculture land prices have exhibited a remarkably strong positive correlation of nearly 89%. The relationship is intuitive: both are scarce assets with constrained supply that serve as long-term monetary hedges. Gold supply grows only about 1–2% annually, while farmland supply is effectively shrinking. As the saying goes, “they aren’t making any more land.”

When investors are seeking stability, capital tends to flow into assets where supply cannot expand. This dynamic was evident following the Global Financial Crisis in 2008 and again during the COVID stimulus cycle in 2020, when both land values and gold prices rose in tandem. Viewed through this lens, the recent rally in gold appears to be moving with land values rather than signaling another leg higher for farmland. Remember that the rise in an asset level, however, does not matter when it comes to year-over-year marketing decisions reliant on cash flow.

Pay Attention to What Matters vs. What Is Interesting

Does the price of gold matter at all to the price you receive for grain? No, but that doesn’t mean you’re going to stop hearing about it. Publications and people on the radio may be asking you to direct your attention to the meteoric rise in gold because it makes great headlines and motivates an audience to do something, when the best course of action may be to simply tune it out.

A situation like the focus on gold and silver is emblematic of our belief that an overabundance of irrelevant information can be distracting and even counterproductive to building a good price for your production. After all, the more you pay attention to factors that don’t matter, the less time you spend focusing on the information that does. Remember, price direction in corn and soybeans is driven by balance sheets, export flows, acreage shifts, yield potential, currency values, and fund positioning — it’s really important that you focus your energy and attention on information that actually has an impact on your markets, not external, unrelated market forces.

At Total Farm Marketing, we have spent forty years helping producers filter out distractions and concentrate on the information that builds price opportunity. If you are looking for a structured, probability-based approach to grain marketing, we would welcome the opportunity to work with you.

Give Total Farm Marketing a call at 800.334.9779 to discuss your situation and how we can help you in your marketing decisions.

©March 2026. Total Farm Marketing. Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. No representation is being made that scenario planning, strategy or discipline will guarantee success or profits. Examples of seasonal price moves or extreme market conditions are not meant to imply that such moves or conditions are common occurrences or likely to occur. Futures prices may have already factored in the seasonal aspects of supply and demand. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing. Total Farm Marketing refers to Stewart-Peterson Group Inc., Stewart-Peterson Inc., and SP Risk Services LLC. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. Stewart-Peterson Inc. is a publishing company. SP Risk Services LLC is an insurance agency and an equal opportunity provider. A customer may have relationships with any of the three companies.

Author

Keegan Madigan