The CME and Total Farm Marketing offices will be closed Monday, May 30, 2022, in observance of Memorial Day

MARKET SUMMARY 5-27-2022

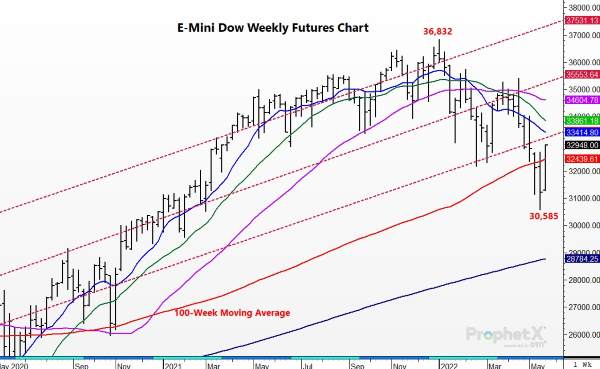

Dow equity futures are looking to snap an 8-week losing streak with Friday’s close. Dow futures were trading higher on Friday, bringing an end to a good week of buying strength in the equity markets. Going into the close, E-Mini Dow equity futures were trading nearly 1700 points higher than last week’s close. This week saw some less concerning news, that brought some short covering and value buying into the markets. A report showing inflation slowing a bit helped give stocks a boost. The core personal consumption expenditures price index rose 4.9% in April, down from the 5.2% pace seen the previous month. This report is watched closely by the Federal Reserve when setting policy. The market’s feeling is if inflation has peaked or is slowing, the aggressiveness of the Fed regarding monetary policy may be less aggressive. In addition, some consumer-based companies report more friendly earnings during the week, which helped ease the nervousness regarding the consumer, which pressured the market last week. The E-Mini Dow futures lost nearly 6,300 points from this year’s high to last week’s low, so a price recovery was welcomed by many. The market may still be vulnerable to more downside pressure, but the turn this week may help turn the charts higher for additional short covering and upside strength.

Like what you’re reading?

Sign up for our free daily TFM Market Updates and stay in the know!

CORN HIGHLIGHTS: Corn futures in the morning trade firmed on short-covering and a recovery in the wheat market ending the session 12-1/4 higher in Jul to close at 7.77-1/4 and 11-1/4 firmer in Dec ending the week at 7.30. For the week, Jul corn futures lost 1-1/4 cents and Dec gave up 2 cents. Losses for two weeks in a row may be signaling upward moment could be shifting, yet a lack of positive new news, planting progress, and a hard slide in wheat prices couldn’t break corn prices. The bulls will argue the market has corrected and is poised to move higher.

In most years, as the end of May approaches if there is a forecast for warmer temperatures and less rain (after rain delays) one might believe there is little hope for prices. That is correct for most years. This year is not like most years. Yet, we will shade our bias to the defensive as there usually just isn’t enough changing weather over the next couple of weeks that suggest the crop is in peril. The key next week may be a better perspective on how many acres may end up as pre-vent plant. We believe that farmers, with expectations for 7.00 plus new crop corn price and the potential for price appreciation, will do all they can to plant corn into late May and early June. The markets are closed on Monday in observance of Memorial Day. Trading will begin on Monday evening at 7:00 PM central. Technically today’s close looks positive, as both old and new crop futures closed above the 50-day moving average. However, the 40, 21, and 10-day averages all help prices in check today.

SOYBEAN HIGHLIGHTS: Soybean futures closed higher again today after yesterday’s huge move up. Higher crude, strong crush basis, and exports to China have all supported this rally. Jul soybeans gained 5-3/4 cents, closing at 17.32-1/4, and Nov lost 3/4 cent at 15.44.

Higher crude gave soybean oil and the entire soy complex a strong rally yesterday, with meal leading the way higher today. The USDA’s cash price for Illinois ended at 433.00 yesterday and Jul meal holds roughly a 5.00 premium over Aug, both bullish signs of demand for meal. The crush margin has begun to narrow as tight supplies of old crop beans have pushed the Jul contract even higher. Jul now holds a 70-cent premium over Aug which has prompted some commercials to start basing cash bids off the Aug contract. Export demand is tightening soybean supply in the U.S. with old crop sales now 46 mb over the USDA’s export estimate with 3 months still to go. China remains the world’s largest buyer and today both Jul soybeans and Sep meal made new highs on the Dalian exchange, with Jul soybeans closing at the equivalent of $22.29 a bushel.

WHEAT HIGHLIGHTS: Wheat futures posted decent gains today as traders began to realize that Russia may not allow Ukrainian grain shipments after all. Jul Chi gained 14-1/4 cents, closing at 11.57-1/2, and Dec up 14-3/4 at 11.73-1/2. Jul KC gained 6-3/4 cents, closing at 12.35-1/4, and Dec up 7-3/4 at 12.48-1/4.

Wheat ended on a positive note after a rocky week. As we mentioned previously, much of the weakness seemed to stem from hopes that Russia would allow Ukraine to export some grain and food. The conversation shifted, however, when Russia clarified that sanctions against them would have to be removed first, making this an unlikely possibility. Ukraine ports are also still closed due to the destruction of infrastructure and mines in the waters. Here in the U.S., the market will need to account for potentially lower HRW and HRS crops due to drought in the former and wet conditions for the latter. The HRS Canadian crop is also at risk due to wet weather. Globally, it was reported that French wheat crop conditions have gotten worse, with the good to excellent rating falling to 69% from 73% previously. This in part helped Paris milling futures to rally another five or so euros today. The main thing that traders should realize is that global wheat supplies are tight and that fact may not change for some time to come. As a reminder, markets are closed Monday in observance of Memorial Day; the Crop Progress report will be released on Tuesday.

CATTLE HIGHLIGHTS: Live cattle futures finished mixed in a quiet trading session for the second consecutive day. The live market traded the opposite of Thursday with light weakness in the front month futures. Feeders were lower, pressured by a firmer corn market tone. Jun cattle finished 0.225 lower to 132.175 and Aug live cattle were 0.200 lower to 132.400. In feeders, Aug feeders lost 0.350 to 166.675. For the week, Jun live cattle were 0.600 higher, and Aug added 0.850. Aug feeders traded 2.400 higher for the last week.

Jun cattle stay tied to the 10 and 20-day moving averages, but softer price action on Friday saw prices close below the 10-day on Friday, which could keep the market susceptible for more downside next week. Jun future posted a bearish reversal on Wednesday, but prices consolidated at the bottom of that range with $132 as support. Cash trade was quiet for the day as trade was wrapped up on the week. Southern trade mostly posted at $137, down $1 from last week’s totals and Northern trade hit $140, with regional reports of strong overall trade values. Retail beef prices ended the week firmer, as midday values traded higher. Choice carcasses gained 0.96 to 264.93 and Select was 2.26 higher to 246.69. Load count was light at 68 loads. Demand was softer this week as retailers moved past the Memorial Day holiday demand. The next target will be purchasing for the 4th of July around the corner. The market was supported this week by a drop in carcass weights. Beef carcass weights are softening, with weights for the week ending May 14 showing steer weights down 7 pounds to 891 pounds, which is 3 pounds below last year. Lighter weights will help tighten the beef production totals. Feeders saw lower trade, influenced by the premium of the Aug contract to the cash index and strong prices in the corn market. Aug is the new lead month and the premium to the cash index is concerning. The Feeder Cash Index was 0.45 higher to 153.80, but trading at nearly a $12.50 discount to the Aug futures. The cattle market is a mix of information, with both supportive and negative factors. That is the reason for some of the choppiness in the cattle market. That choppiness will likely continue going into the 3-day holiday weekend.

LEAN HOG HIGHLIGHTS: Hog futures finished mixed to end the week on choppy trade and position squaring as the market set up for the 3-day weekend. Jun hogs finished 0.700 lower to 110.400 and Jul hogs slipped 0.100 to 111.725. For the week, Jun hogs gained 1.525 and Jul added 2.725 as prices closed higher for the second consecutive week.

Jun hog futures are still held in check by the 100-day moving average over top of the market, trading at 111.430 on Friday. This was the fourth test of this barrier in the past five sessions. If prices could work through this point, the 50% retracements of the recent sell-off from the April highs are at the $112.000 level. The midday cash market saw a softer tone at midday. Midday direct trade was 2.80 lower with the weighted average at 108.54 and the 5-day average moved faded to 111.08. The CME Lean Hog Index is reflecting the higher cash tone overall this week and gained 0.53 to 104.40. The index traded 4.03 higher for the week. The premium of the Jun contract is concerning, and the new term upside may be limited by the 6.000 gap between the two. Retail values trended higher at midday with carcass values 0.39 higher to 108.52. Movement was good at 182 loads. Pork carcass values trended higher as Friday’s midday trade was $1.50 higher than Monday’s close. The CME Pork Cutout Index added 0.83 to 107.55 reflecting the recent strength. The rally is taking a pause but trying to push to another level, but the 100-day moving average is a strong barrier. Market fundamentals are staying favorable and may be enough to move prices higher for the next leg. The trend early next week will be a key.

DAIRY HIGHLIGHTS: The Class IV milk trade has caught a bid the past couple weeks, as butter and powder prices once again soar in the United States. Over the past two weeks, US butter has gained 17.25c to $2.8775/lb, while US powder has added 13c to $1.86/lb. Neither market has had enough strength to push into new highs for the year, but the demand surge has brought these products within striking distance of new highs. The turnaround in demand for these products has taken Class IV milk up into new all-time highs. June 2022 Class IV milk added 50c this week to $25.55, after having added $1.05 last week. The contract that set the record this week is the July contract, which added 55c this week to $25.75.

Total Farm Marketing and TFM refer to Stewart-Peterson Group Inc., Stewart-Peterson Inc., and SP Risk Services LLC. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of the National Futures Association. Stewart-Peterson Inc. is a publishing company. SP Risk Services LLC is an insurance agency. A customer may have relationships with all three companies. TFM Market Updates is a service of Stewart-Peterson Inc. Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition.

Author

John Heinberg