MARKET SUMMARY 4-20-2022

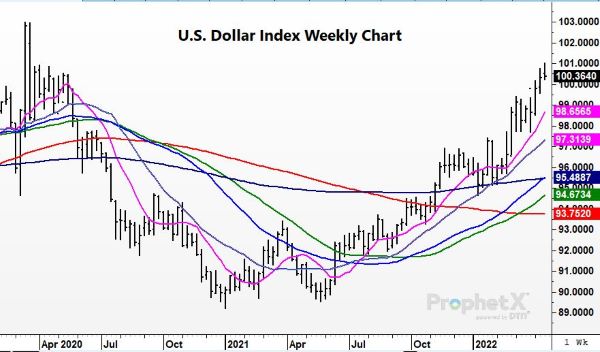

The U.S. dollar index is trading at its highest levels in two years, as the dollar has maintained its trend higher. Since last April, the U.S. Dollar has been trending higher and crossed over the 100-basis point level this week. The rally has netted an 11.00 basis point gain in the index since the rally started. The main driver behind the dollar strength has been the concern of monetary policy and rising interest rates as the fed is trying to handle the inflationary environment. The Federal reserve has started to raise interest rates, and the bond market is pricing in the potential for additional rate hikes in the futures. The strong inflationary environment and the surge in commodity values has only added to the strong inflation outlook for the future. The dollar index will likely trend higher overall but is still not a limiting factor for the demand of most U.S. commodities as concerns for food security are outweighing the costs on U.S. products in the export market.

Like what you’re reading?

Sign up for our free daily TFM Market Updates and stay in the know!

CORN HIGHLIGHTS: Corn futures had an impressive close today, gaining 11-3/4 in May 10-1/4 in July, and 1-1/2 in December. July closed at 8.10, a new contract high close, and December finished at 7.48-1/2 just under the previous contract high close of 7.49-3/4 from Monday. Prices finished will off the daily low by just under 20 cents for the old and 10 cents for new. Strength in soybeans and meal, rain delaying planting, and growing concern that some parts of Brazil are forecasted to remain dry and on the warm side as the crop heads towards pollination. Today’s finish was impressive considering over bought technical conditions and a sell signal in stochastics were ignored. Traders took this morning’s dip as an opportunity to buy.

We indicated earlier in the week a growing reality that Ukraine may not be much of a participant exporting last year’s crop or growing this year’s crop, especially for exports. That is becoming more real daily. For lack of better words that region of the world is a mess. On April 20, we are still not convinced that wet weather delays are a major issue for the Midwest. However, they are noted. Cool temperatures have been problematic as well, but it will warm up. On the other hand, critically dry regions down in the Texas Panhandle area could be problematic for this year’s crop production, especially regions that may not have irrigation, or even for areas that have irrigation but may be lacking water.

SOYBEAN HIGHLIGHTS: Soybean futures posted new contract high closes for both old and new crops. May gained 30-1/4 cents to end the session at 17.46-3/4 and November added 9-0 cents to close at 15.29-1/2. Strong gains in meal and oil along with talk of China buying more soybeans were supportive. Short covering was likely a feature today. Limited farmer selling is also suggesting little old crop is in the hands of farmers. Firmer energy prices and a drop in the dollar today were also viewed as supportive.

With November soybean futures finding new life there is little doubt the market is trying to fight for acres. Recent strong gains in corn prices since the March 31 Acreage report and a current ratio of 2.04 November soybean futures divided by December corn futures suggests that soybeans could be a tight supply. Typically, if the ratio is below 2.45 it suggests that farmers may lean toward more corn in their acreage mix. Just as important, continued talk that China could be a buyer in the days ahead is fueling speculative support for price. China’s hog herd remains as large or larger than pre-pandemic levels and limited supply availability of soybeans out of South America indicate the U.S. could likely experience more importers buying. Bottom line is the USDA may raise exports and reduce ending stocks. At the same time, the market is anticipating some acreage switch from soybeans to corn. Meal futures prices began today 4.00 to 6.00 below cash prices; therefore, today’s gains in futures by 5.00 to 6.00 is not a surprise.

WHEAT HIGHLIGHTS: Wheat futures traded lower today likely due to profit taking and overbought conditions, along with a lack of fresh news. Though they did settle in the red, it was noted that futures closed well off daily lows. May Chi lost 11 cents, closing at 10.88 and July down 11-1/2 at 10.97-1/2. May KC lost 8-1/4 cents, closing at 11.63-1/4 and July down 6-3/4 at 11.69-1/2.

According to Reuters, 11 million people in Ukraine have been displaced by the war. It is not clear if that means they have actually left the country, but in any case, they are not where they are supposed to be. With a population of about 44 million, that is 1 in 4 Ukrainians, raising serious questions about their labor force this season. This will impact not only agriculture production, but logistics like trucking and shipping as well. Russia is said to be launching a new offensive in eastern Ukraine, which will only make the situation more serious. On a bearish note, the IMF (International Monetary Fund) lowered their estimate of world GDP growth from 4.4% to 3.6%. This raises concerns about economic development as well as demand for energies and commodities. Wheat prices specifically seem to be waiting for the next big headline to provide direction. Both the 6-10 and 8-14 day forecasts show dry weather across most of the US southern plains. In other wheat related news, Egypt, which sourced 80% of their wheat from Russia and Ukraine last year, has approved India as an origin for wheat. However, India will be required to meet strict quality standards. Despite sanctions against them, Russia is reportedly still exporting wheat as well.

CATTLE HIGHLIGHTS: Cattle futures finished strongly higher as cash market strength and technical buying supported the cattle markets. Apr live cattle gained 1.725 to 143.075, and June added 2.050 to 138.625. For feeders, May rallied 1.700 to 162.475.

The most actively traded June contract worked higher on Wednesday as cash trade brought buyers into the market. June futures closed back above the 100-day moving average, and with the strong price action, are open to challenge the 140.00 level or higher. Cash trade began to build on Wednesday with southern live deals marked at $139 to $141, mostly $140, $1 higher than last week’s weighted averages. In the North at $228 to $236, mostly $230, $4 higher than last week’s weighted averages. Some regional packers saw strong bids to 146 in Nebraska, but the higher trend is well established. Beef cutouts were softer at midday (Choice 269.59 -0.34; Select 256.81 -2.40), with improved box movement of 97 loads. The market will get more demand news with the weekly export sales report on Thursday morning. The feeder market saw buying strength supported by the live cattle strength, and a softer early tone in the grain markets. Feeder markets saw good price action, but the movement of grain prices are likely to impacts the strength in feeders. Apr feeders are still tied to the index, gained 0.17 to 154.66 but is running at a discount to front-month futures and could be a limiting factor. Cattle on Feed report is Friday this week, and the market is expecting to see feeder placement decline year-over-year, which could support Feeder prices. Overall expectations for the report are: Total cattle on Feed at 100.4%, Placements at 92.2%, and Marketing at 98.2% of last year. Cash market strength has brought buying optimism into the cattle markets at mid-week. Technically, charts are improved, and buyer should stay active in the market going into the Cattle on Feed report at the end of the week.

LEAN HOG HIGHLIGHTS: Bear spreading remained the theme in the hog futures market, as the premium of futures to the cash market weighed on front month contracts and posted triple-digit losses. May hogs lost 2.225 to 112.475, and the more actively traded June contract lost 2.575 to 118.750.

The selling pressure in the front end of the market is trying to tighten the premium to the cash market. June hogs are weak technically and look to be ready to challenge support at the 108.000-110.000 level. This price area will be a key level to help maintain the current uptrend in the market. The cash market has been a concern, but midday values saw some strength on Tuesday, but prices were softer on Wednesday. National Direct midday values were .67 lower compared to Tuesday, and the weighted average price was 99.02 and the 5-day average firmed to 97.92. The Lean Hog Index was softer losing .35 to 99.98. The deferred futures premium over the index is concerning and a limiting factor, as May is holding a 12.495 premium to the index. Pork carcasses showed higher midday trade. Pork carcasses were 2.82 higher to 109.94, rebounding after Tuesday’s disappointing close. The load count light at 156 loads. USDA will release weekly export sales on Wednesday morning, and that could help provide direction in the market for the end of the week. The hog market might be trying to find some equilibrium and balance in price values. Supported by strong demand, front-end hog prices are lofty compared to the current cash. Deferred futures may not be reflecting the true picture of the hog market supply and may be undervalued. The bear spreading will likely stay the theme in the market in the short-term.

DAIRY HIGHLIGHTS: There was steady offering in both class III and IV milk futures on Wednesday ahead of this afternoon’s Milk Production report. The market was still reacting to a bearish GDT auction event from Tuesday that was followed by a US spot market that had each individual product close lower. There was pretty heavy offering again today in the US spot market with cheese blocks down 2.50c and barrels down 5.25c. The powder market fell 0.50c, while whey was unchanged. The lone product to close green was butter, which added 0.25c up to $2.72/lb. The spot cheese trade has closed red two days in a row and looks like it could continue lower in the short run.

Total Farm Marketing and TFM refer to Stewart-Peterson Group Inc., Stewart-Peterson Inc., and SP Risk Services LLC. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of the National Futures Association. Stewart-Peterson Inc. is a publishing company. SP Risk Services LLC is an insurance agency. A customer may have relationships with all three companies. TFM Market Updates is a service of Stewart-Peterson Inc. Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition.

Author

Brandon Doherty