Information produced by ADM Investor Services, Inc. and distributed by Stewart-Peterson Inc.

Wheat prices overnight are down 5 in SRW, down 8 1/2 in HRW, down 5 3/4 in HRS; Corn is down 3 1/4; Soybeans down 11 1/4; Soymeal down $0.60; Soyoil down 0.30.

Markets finished last week with wheat prices down 7 1/4 in SRW, down 4 1/4 in HRW, down 5 1/4 in HRS; Corn is down 2; Soybeans down 32 1/4; Soymeal down $1.86; Soyoil down 1.40.

For the month to date wheat prices are down 55 1/2 in SRW, down 47 3/4 in HRW, down 31 3/4 in HRS; Corn is down 5 1/2; Soybeans down 28 3/4; Soymeal down $13.30; Soyoil down 2.40.

Year-To-Date nearby futures are down 7.0% in SRW, down 5.5% in HRW, down 3.4% in HRS; Corn is down 0.8%; Soybeans down 1.6%; Soymeal down 4.3%; Soyoil down 3.4%. Malaysian markets are closed for Holiday.

Like what you’re reading?

Sign up for our other free daily TFM Market Updates and stay in the know!

China markets are closed this week for Holiday.

There were changes in registrations (-4 SRW Wheat, -46 Soybeans) Registration total: 2,783 SRW Wheat contracts; 0 Oats; 154 Corn; 1,094 Soybeans; 479 Soyoil; 62 Soymeal; 280 HRW Wheat.

Preliminary changes in futures Open Interest as of January 20 were: SRW Wheat up 2,189 contracts, HRW Wheat up 4,680, Corn up 1,677, Soybeans up 2,266, Soymeal down 1,109, Soyoil up 9,420.

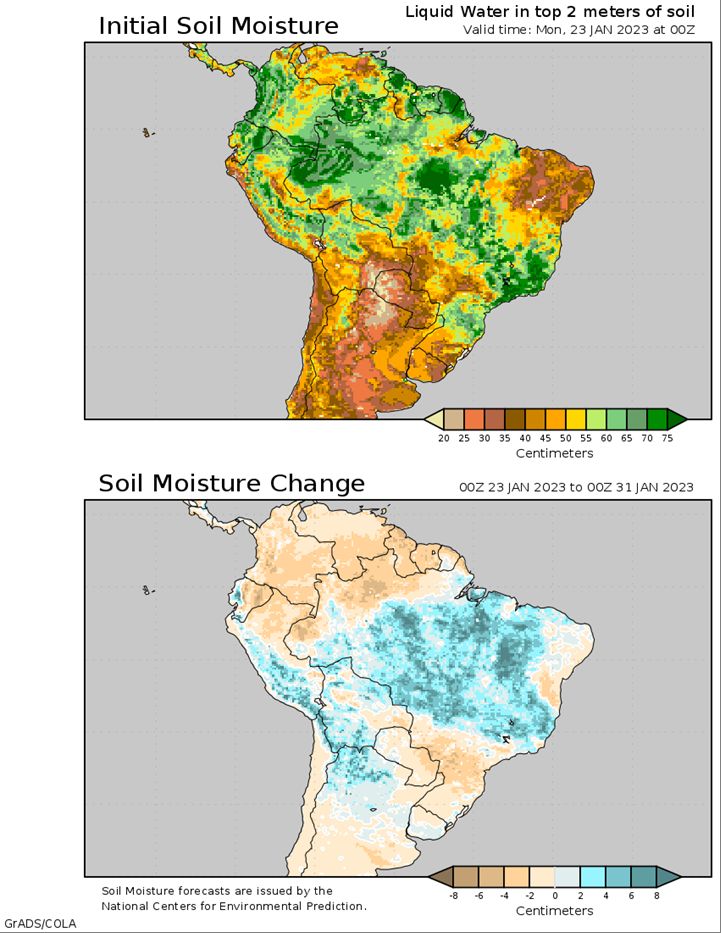

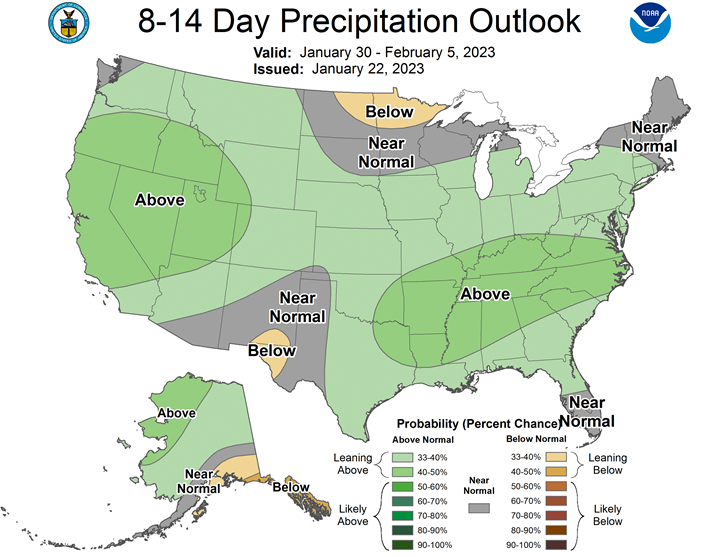

Brazil Grains & Oilseeds Forecast: A front moved through southern areas this weekend, but dryness is taking a hold of the region yet again until another front moves through this weekend. Models disagree, but could linger that front in the region next week, which would be helpful for filling corn and soybeans. Widespread precipitation elsewhere continues to favor later-planted soybeans, but is delaying harvest a little. If the wetness continues too long, it may push back the safrinha corn planting schedule, which would not be an ideal scenario for the crop.

Argentina Grains & Oilseeds Forecast: A front moved through over the weekend with scattered showers. A lot of 0.75-1.5″ reports were received, but the crop is in deep drought and crop conditions continue to be very poor. Another couple of fronts will move through this week, which may not be as organized as the last front, but are still forecasting similar amounts for the week. Should amounts disappoint, the region would have to wait until the middle of next week for the next chance of rain. If the forecasts hold, stabilization of the corn and soybean crops are likely, but a stark turnaround may not occur.

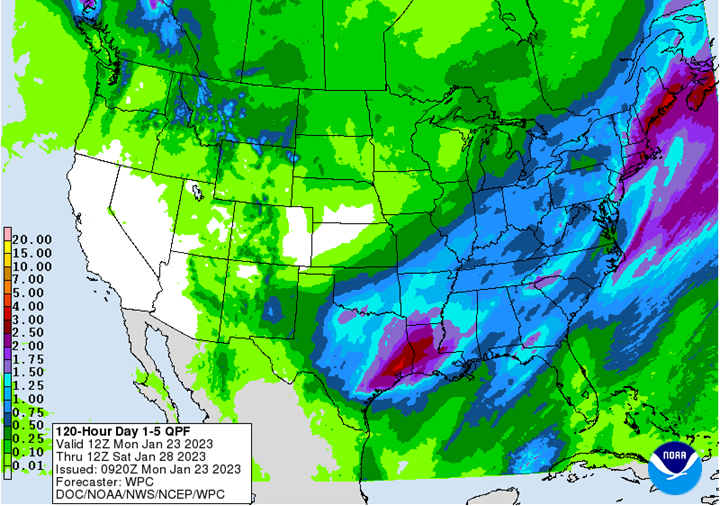

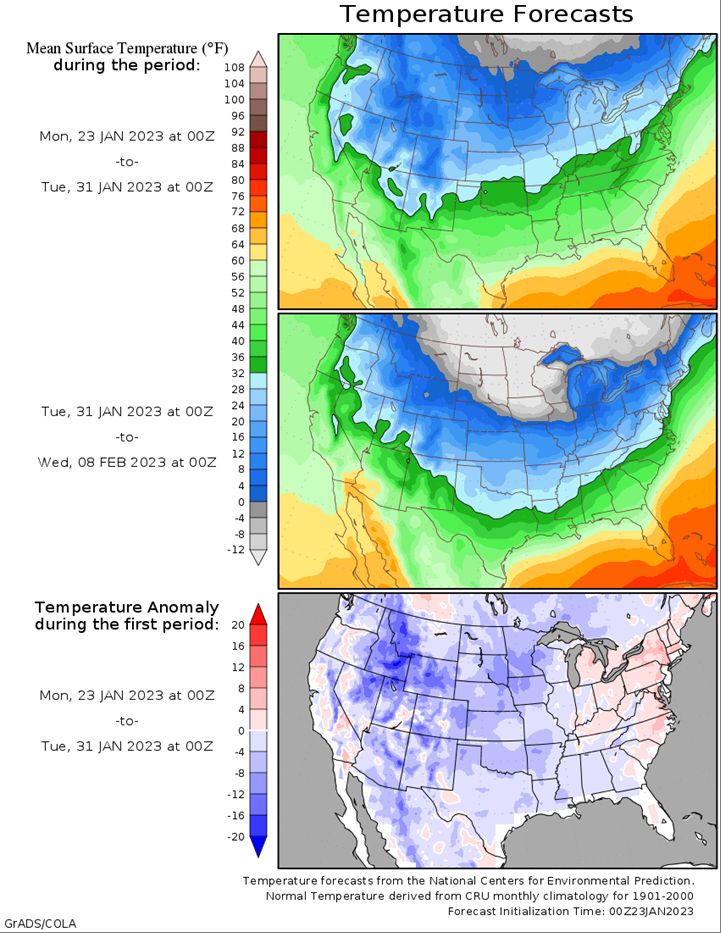

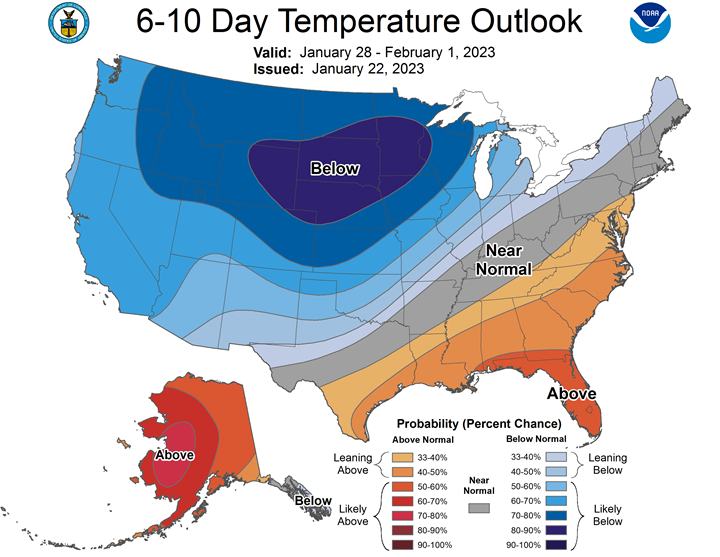

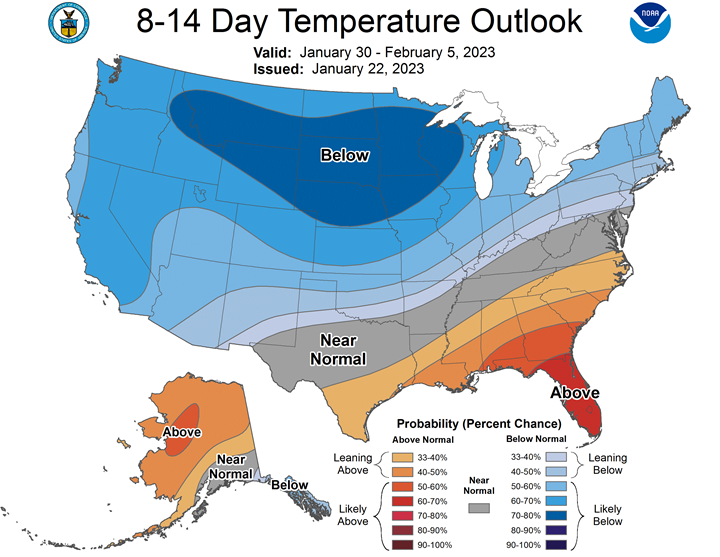

Northern Plains Forecast: A cold front will push through the region late this week that will bring in much colder air for the end of January and the beginning of February, leading to increased stress for livestock.

Central/Southern Plains Forecast: A system brought scattered showers to the region over the weekend, including a band of moderate to heavy snow from Colorado through Kansas. Another system will move out of the Rockies and through Texas Monday night and Tuesday, with widespread precipitation, including a band of moderate to heavy snow across northern Texas, Oklahoma, and southern Kansas. This is the best chance for precipitation this region has seen in a long time. A front will move into the region this coming weekend and may provide some additional showers, but temperatures will fall dramatically behind the front.

Midwest Forecast: A system moved through over the weekend with widespread showers across the southeastern half of the region, and a couple of bands of moderate snow. A stronger system will bring another band of moderate to heavy snow for southeastern areas Tuesday night and Wednesday. A clipper will bring a strong cold front into the region later this week that will send temperatures well below normal. The front will be pushed southward a couple of times by additional systems over the weekend and next week. Each will bring precipitation with them and push the colder air deeper through the region.

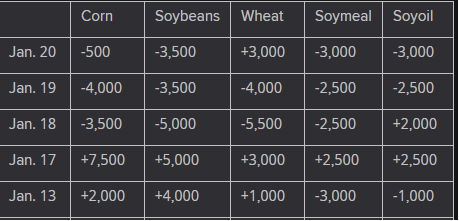

The player sheet for Jan. 20 had funds: net buyers of 3,000 contracts of SRW wheat, sellers of 500 corn, buyers of 3,500 soybeans, sellers of 3,000 soymeal, and sellers of 3,000 soyoil.

TENDERS

- SOYBEANS SALE: U.S. exporters sold 220,000 tonnes of soybeans for delivery to unknown destinations during the 2022/2023 marketing year, the U.S. Department of Agriculture said Friday.

PENDING TENDERS

- RICE TENDER: South Korea’s state-backed Agro-Fisheries & Food Trade Corp issued an international tender to purchase an estimated 113,460 tonnes of rice to be sourced from the United States. The deadline for submissions of price offers was Dec. 29.

- FEED WHEAT AND BARLEY TENDER: Japan’s Ministry of Agriculture, Forestry and Fisheries (MAFF) said that it will seek 70,000 tonnes of feed wheat and 40,000 tonnes of feed barley to be loaded by Feb. 15 and arrive in Japan by March 16, via a simultaneous buy and sell (SBS) auction that will be held on Jan. 25.

- SOYBEAN TENDER: South Korea’s state-backed Agro-Fisheries & Food Trade Corp issued international tenders to purchase around 19,000 tonnes of food-quality soybeans free of genetically-modified organisms (GMOs).

US BASIS/CASH

- Basis bids for corn and soybeans shipped by barge to the U.S. Gulf Coast were relatively steady on Friday, as traders anticipated slowing demand ahead of the Lunar New Year holiday, dealers said.

- CIF Gulf soybean barges loaded in January were bid on Thursday at 110 cents over March, steady from Thursday. February soy barges slipped down 2 cents, bid at 98 cents over March futures.

- FOB offers for February soybean shipments were steady at about 130 cents over March.

- Corn barges loaded in January were bid at 75 cents over March, down 1 cent from Thursday. February corn barges were bid at 82 cents over March futures, steady from the day prior.

- FOB offers for February corn shipments were around 88 cents over March futures, steady from Thursday.

- Spot basis bids for soybeans were mixed at terminals along rivers around the U.S. Midwest on Friday, dealers said.

- The soy basis was steady to firm at interior elevators, rising by 5 cents a bushel in the Chicago area, and flat at processors.

- Cash bids for corn were steady to weak along rivers, and steady to firm at processors.

- At interior elevators, corn bids were unchanged.

- Farmer sales of both commodities were slow, with growers holding out to see if prices rebound to test recent highs before making decisions on new contracts, dealers said.

- Spot basis bids for corn and soybeans were steady to firm at U.S. Midwest river terminals on Thursday morning, grain dealers said.

- Around the interior, the basis for both commodities also was steady to firm at elevators, rising in Cincinnati, Ohio.

- Processor bids for soybeans and corn were mostly unchanged.

- At ethanol plants, the corn basis was flat.

- Farmer selling was slow, a dealer in Council Bluffs, Iowa, said.

- Growers had booked a good amount of soybean sales earlier this week when futures rallied to their highest in nearly seven months and were waiting to see if prices eclipsed that recent top before committing to new deals, the dealer added.

- Winter storms this week slowed deliveries of supplies from previously booked contracts at grain terminals in the western half of the region.

- Although the corn basis was mostly flat at processors, bids rose by 20 cents a bushel in Blair, Nebraska.

- Spot basis bids for hard red winter wheat held steady at rail and truck market terminals across the southern U.S. Plains on Friday, grain dealers said.

- Protein premiums for hard red winter wheat delivered by rail to or through Kansas City rose by 15 cents a bushel for wheat with protein content ranging from 12.6% through 14%, according to CME Group data.

- Spot basis offers for U.S. soymeal were unchanged at rail and truck market processors on Friday, dealers said.

- Concerns about tight supplies were the dominant market factor, a rail broker said.

- Some plants in Iowa shut down earlier this week for emergency maintenance and were still trying to catch up on providing supplies to fill previously booked contracts.

- There were no listed offers at those plants, a dealer in that area said.

- Additionally, a plant in Fairmont, Minnesota, was expected to be shuttered for maintenance, the rail broker said.

- The tight supply base also affected the CIF market for soymeal shipped by barge to the U.S. Gulf and FOB offers for soymeal loadings onto ocean-going vessels at the export terminals.

- There were no CIF or FOB offers listed until March.

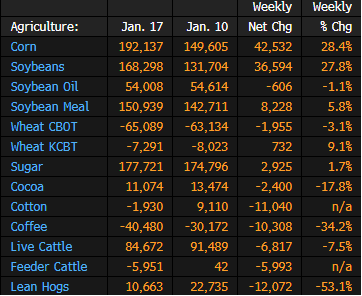

CFTC Money Managers’ Commodity Positions for Jan. 17

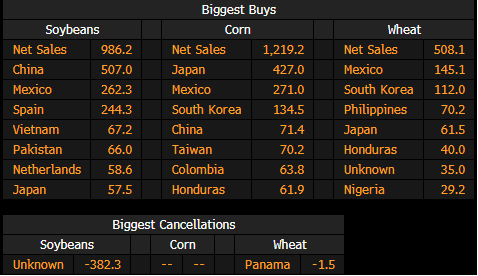

US Agriculture Export Sales for Week Ending Jan. 12

US Export Sales of Soybeans, Corn and Wheat by Country

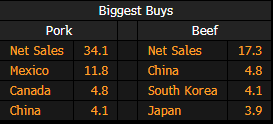

US Export Sales of Pork and Beef by Country

The following table shows US export sales of pork and beef product by biggest net buyers for week ending Jan. 12, according to data on the USDA’s website.

- Mexico bought 11.8k tons of the 34.1k tons of pork sold in the week

- China led in beef purchases

US Cattle on Feed Fell to 11.68M Head on Jan. 1

Brazil May Export 93M Tons of Soy in 2023: Safras

Compares with 78.9m tons estimated for 2022, consultancy firm Safras & Mercado says in an emailed report.

- Projection indicates an increase of 18% between seasons

- Total supply of soybeans should increase by 16%, to 157.2m

- Total demand is projected at 148.5m tons; +12% y/y

- Safras sees crushing of 52m tons in 2023 and 50m tons in 2022; 4% of growth

- Imports of 100,000 tons for 2023, down 76% over 2022

Argentine government, farm exporters seek relief from historic drought

Argentine Economy Minister Sergio Massa met with agricultural exporters on Friday to analyze and “seek solutions” to help the country’s key grain industry after it was hammered by the worst drought the country has faced in at least 60 years.

The dry spell is contributing to a broader economic slump battering the South American country, marked by sky-high inflation and a weakening local currency.

Massa said he would meet with farmers over the next week, and by the beginning of February expected to have prepared some answers for farmers struggling with dry soil resulting from a drought that began in May.

Lack of rainfall almost halved wheat output this cycle and hampered production of the current soybean and corn crops, though local grains exchanges predict fresh rains could bring some relief in coming days.

Argentina is the world’s leading exporter of soybean oil and meal and the third largest exporter of corn, as well as a major wheat supplier. Its production is being closely watched after Russia’s invasion of Ukraine prompted major disruptions and spiking prices in the grains market.

“We understand that there are things that we will be able to resolve and others that we will not,” said Massa in a statement, adding that a shared effort would have to be made between the government and farm sector leaders.

Massa also highlighted that Argentina’s agro-industrial sector had pushed its exports to record levels last year.

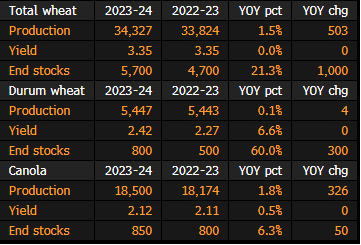

Canada 2023-24 Crop Production, Reserves Estimates: AAFC

The following table is a summary of principal crop estimates, according to Agriculture and Agri-Food Canada, the nation’s agriculture ministry. Level figures are in thousands of tons, yields in tons per hectar.

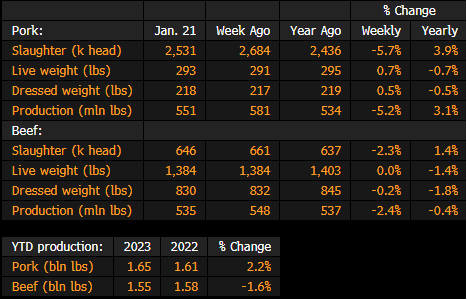

US Pork Production Falls 5.2% This Week, Beef Down: USDA

US federally inspected pork production falls to 551m pounds for the week ending Jan. 21 from 581m in the previous week, according to USDA estimates published on the agency’s website.

- Hog slaughter down 5.7% from a week ago to 2.531m head

- Beef production down 2.4% from a week ago, cattle slaughter falls 2.3%

- For the year, beef production is 1.6% below last year’s level at this time, and pork is 2.2% above

SOYBEAN/CEPEA: High demand raises prices in the USA, but record harvest in BR constrains rises

Soybean Futures have increased at CME Group (Chicago Mercantile Exchange) this week, boosted by the firm demand from abroad and unfavorable weather in Argentina. Also, the low surplus of the 2021/22 crop in Brazil led importers to the USA. However, international valuations were limited by the dollar appreciation and expectations for a record harvest in Brazil (the number one producer and exporter of soybean in the world).

Still, this week, the Mar/23 contract surpassed USD 15/bushel, a nominal record compared to that in the same period of previous years. On Thursday, 19, this contract closed at USD 15.1475/bushel (USD 33.39 per 60-kg bag), 1.5% up from that on the previous Thursday, 12. The US dollar rose 1.6%, to BRL 5.175 on Thursday, 19.

According to the USDA, the American exports of soybean increased 42.48% in the two last weeks.

In Brazil, quotations did not rise, however, international valuations and the dollar appreciation limited steeper decreases. On the average of the regions surveyed by Cepea, soybean prices dropped 0.3% in the over-the-counter market (paid to farmers) and 0.6% in the wholesale market (deals between processors). In the same period, the ESALQ/BM&FBovespa Paranaguá (PR) Index decreased 0.3%, to BRL 176.93 (USD 34.19) per 60-kilo bag. The CEPEA/ESALQ Paraná Index rose 0.3%, closing at BRL 171.10 (USD 33.06) per 60-kilo bag on Thursday, 19.

CROPS – The soybean harvesting continues slow in Mato Grosso (Brazil’s major soybean-producing state), since high moisture is hampering crop activities. According to Imea, 2.4% have been harvested in the state, less than the 4.2% in the same period last year and the 3.6% on the average of the last five years.

In Rio Grande do Sul, 98% of the soybean crop had been sown by Jan. 19th, with 78% of the total still in the vegetative development stage.

CORN/CEPEA: Weak demand in Brazil presses down quotations

Not even the high volumes exported and corn valuations abroad and at Brazilian ports were enough to underpin prices in the Brazilian market, where quotations are fading in most of the regions surveyed by Cepea. Price drops are a reflex of Brazilian purchasers’ low interest in buying corn for the short term, besides some sellers’ needs for trading and making room in warehouses.

Although Conab’s estimates released on Jan. 13th pointed to lower stocks (-2 million tons), at 5.28 million tons, high expectations for the soybean and corn crops, whose harvestings are supposed to step up in the coming weeks, are making farmers more willing to lower asking prices.

Aware of the current scenario, purchasers close deals only when prices are attractive to them, keeping pressure on quotations. In Campinas (SP), the ESALQ/BM&FBovespa Index for corn decreased 1.7% in the last seven days, to BRL 85.38 (USD 16.50) per 60-kilo bag on Thursday, 19.

On the average of the regions surveyed by Cepea, prices dropped 0.1% in the over-the-counter market (paid to farmers) and 0.8% in the wholesale market (deals between processors).

PORTS – Opposite to the observed in the domestic market, the international demand for the Brazilian corn has been high, and the prices at ports have resumed increasing this week. Besides higher demand, the dollar appreciation and valuations abroad – which raise the export parity value – influenced these increases too.

In seven days, the prices of the product delivered at the ports of Paranaguá (PR) and Santos (SP) rose 2.8% and 0.4%, averaging BRL 89.7 and BRL 88.54/bag on Thursday. The dollar valued 1.6%, closing at BRL 5.175 on Jan. 19th.

CROPS – The harvesting of the summer crop has begun in more Brazilian regions, and sowing of the second crop is in progress, due to the advance in the soybean harvesting. As for the summer crop in Rio Grande do Sul, 95% had been sown by Jan. 19th, while 18% have been harvested.

In Paraná, the harvesting of the summer crop is beginning. In São Paulo and Minas Gerais, activities have begun too, according to Cepea collaborators. The second crop has begun in Mato Grosso, and activities advanced slightly in Paraná this week. With rains in many Brazilian regions, farmers are optimistic.

Urea, Potash Remain Pressured; Phosphates, Sulfur Rebound

Prices for nitrogen and potash remained under pressure. Urea was down at most inland US terminals despite an increase of $10 a short ton (st) at New Orleans (NOLA), with Western Canada urea falling $100 a metric ton or more since December. Urea ammonium nitrate dropped $70-$80/st at NOLA and inland, while potash slid $10-$15/st at NOLA and even more in most inland markets as producers offered winter fill programs to entice buyers.

Despite a drop in monoammonium phosphate (MAP) prices in the Western US and Western Canada, diammonium phosphate (DAP) prices moved up at NOLA and in the Corn Belt as supplies tightened in advance of spring demand. A tighter sulfur market due to refinery maintenance and cold-weather outages also pushed Tampa sulfur prices higher for 1Q contracts.

Brazil Urea, Potash Stable; Phosphates Mixed on Slow Demand

Brazil urea narrowed to $450-$455 a metric ton (mt) vs. last week’s $445-$460, with inland prices largely unchanged, as the focus shifts to demand for the 2024 safrinha season. Ammonium sulfate slipped to $240-$250/mt vs. last week’s $245-$250, with inland prices falling $10/mt as blenders look to urea for their nitrogen content. Phosphate prices edged higher to $650-$670/mt vs. last week’s $650-$665, while inland prices dropped $10-$25 a short ton amid slower demand. Despite hopes for firming potash prices due to higher demand, the market remained at $500-$520/mt amid an influx of lower-priced tons from Belaraus. Inland potash prices were down $10-$25.

SOUTH AMERICA

UNITED STATES

This commentary is provided by ADM Investor Services, a futures brokerage firm and wholly owned subsidiary of ADM Company. ADMIS has provided expert market analysis and price risk management strategies to commercial, institutional and individual traders for more than 50 years. Please visit us at www.admis.com or contact us at sales@admis.com to learn more.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by Archer Daniels Midland Company. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS.

| CONFIDENTIALITY NOTICE

This message may contain confidential or privileged information, or information that is otherwise exempt from disclosure. If you are not the intended recipient, you should promptly delete it and should not disclose, copy or distribute it to others. |

Author

ADM Investor Services, Inc.