Information produced by ADM Investor Services, Inc. and distributed by Stewart-Peterson Inc.

Wheat prices overnight are up 10 1/4 in SRW, up 7 1/2 in HRW, up 4 3/4 in HRS; Corn is up 1 1/2; Soybeans up 6 1/2; Soymeal up $0.32; Soyoil up 0.12.

For the week so far wheat prices are up 19 3/4 in SRW, up 22 in HRW, up 7 3/4 in HRS; Corn is down 1/2; Soybeans up 15 1/2; Soymeal up $1.37; Soyoil up 0.27.

For the month to date wheat prices are up 8 3/4 in SRW, up 13 in HRW, up 8 1/2 in HRS; Corn is up 2 3/4; Soybeans down 11 1/4; Soymeal up $3.70; Soyoil down 1.42.

Like what you’re reading?

Sign up for our other free daily TFM Market Updates and stay in the know!

Year-To-Date nearby futures are down 2.8% in SRW, up 0.4% in HRW, down 1.0% in HRS; Corn is up 0.6%; Soybeans up 0.4%; Soymeal up 1.8%; Soyoil down 4.6%.

Chinese Ag futures (MAR 23) Soybeans up 53 yuan; Soymeal down 3; Soyoil down 186; Palm oil down 120; Corn up 4 — Malaysian palm oil prices overnight were down 64 ringgit (-1.68%) at 3751.

There were no changes in registrations. Registration total: 2,728 SRW Wheat contracts; 0 Oats; 154 Corn; 797 Soybeans; 479 Soyoil; 52 Soymeal; 192 HRW Wheat.

Preliminary changes in futures Open Interest as of February 1 were: SRW Wheat up 2,069 contracts, HRW Wheat up 202, Corn up 616, Soybeans up 679, Soymeal down 602, Soyoil up 8,990.

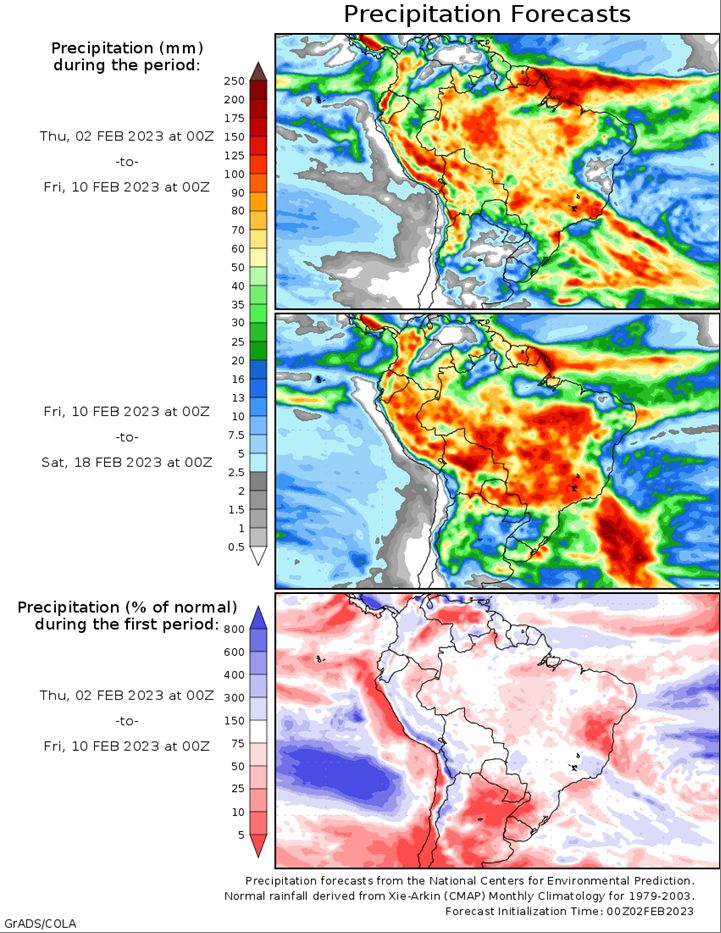

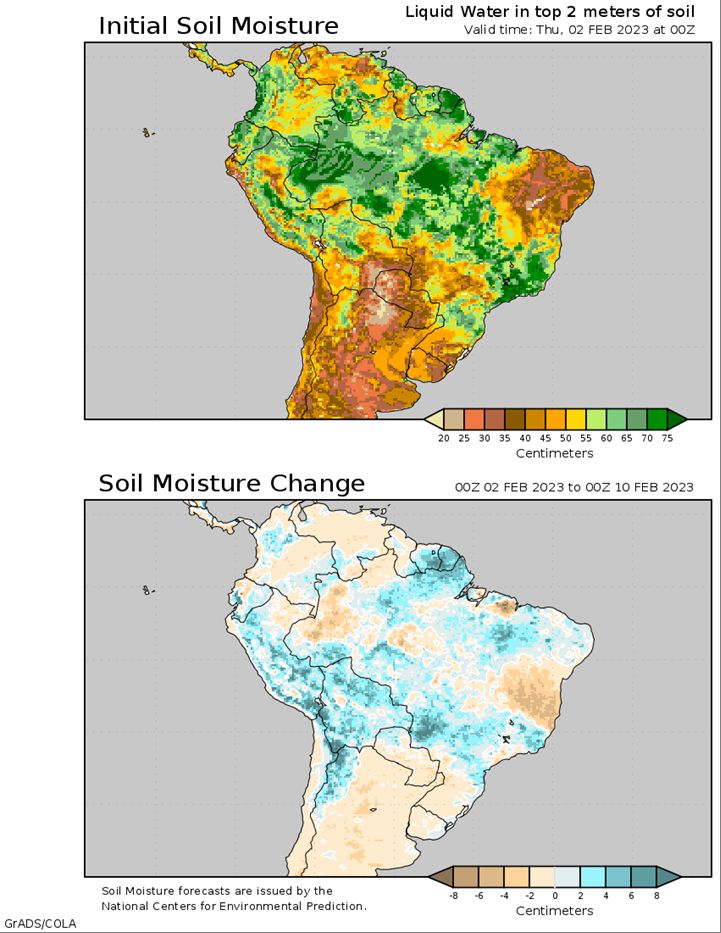

Brazil Grains & Oilseeds Forecast: Central and northern Brazil will continue to see showers throughout the week, but there should be some breaks to complete some soybean harvest and safrinha corn planting from Mato Grosso to Minas Gerais. Rains become heavier again next week, which will set the table for more delays. The far southern state of Rio Grande do Sul remains mostly dry, however, with only limited chances for rain as a front moves through Thursday and Friday.

Argentina Grains & Oilseeds Forecast: A front will pass through Argentina with scattered showers through Thursday, but showers may again miss some key areas. The country’s primary growing areas will be in a stretch of drier weather again until about mid-February when the next significant front moves through. That dryness may undo the beneficial effects from recent rainfall.

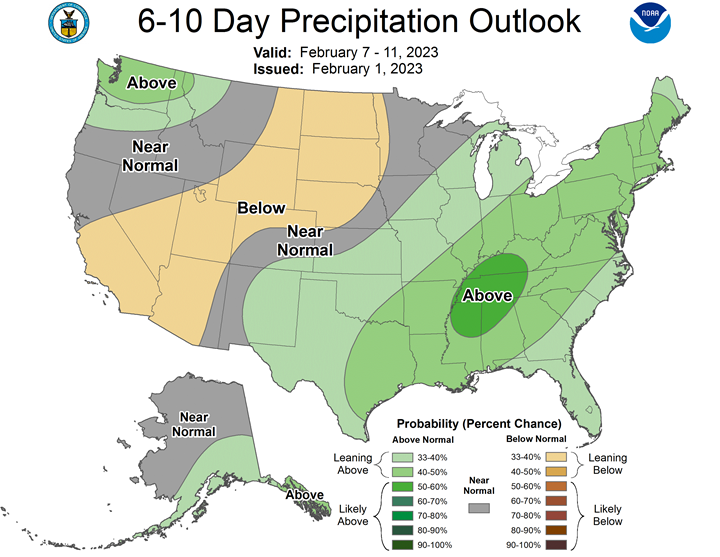

Northern Plains Forecast: Very cold air in the Northern Plains and Canadian Prairies will be replaced by some warmer air in the next couple of days. Above-normal temperatures forecast for the following week will reduce stress on livestock.

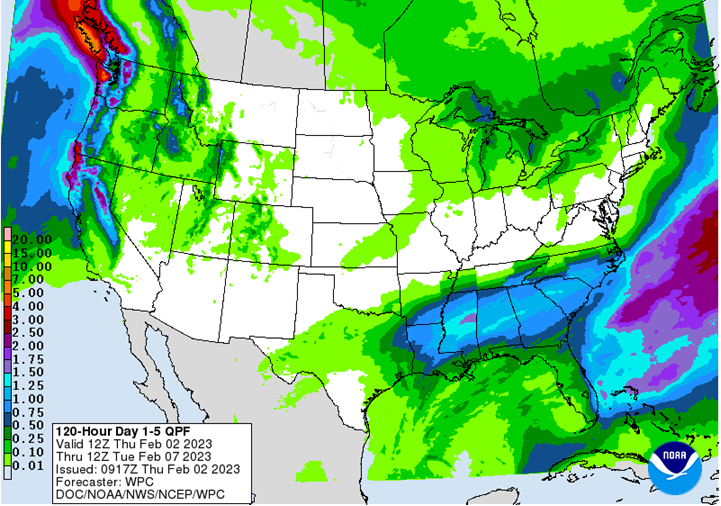

Central/Southern Plains Forecast: Temperatures will be rising in the Central and Southern Plains going into the weekend. Southern areas will see precipitation continuing through Thursday and will be cold enough for some freezing rain and snow accumulations in some areas. Drought areas in Oklahoma and Texas will see some precipitation, but not enough to turn the drought around in a meaningful way.

Midwest Forecast: It will be drier and cold in the Midwest for the rest of the week, with lake-effect snow late Thursday into Friday with another push of cold air. The cold will be brief though, as warmer air will build back into the region over the weekend. Another system will move through early to mid-next week, but temperatures behind the system will continue to be mild.

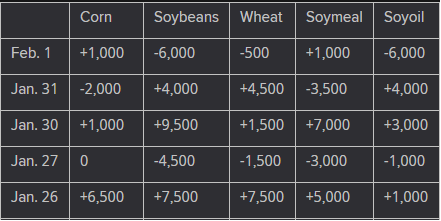

The player sheet for Feb. 1 had funds: net sellers of 500 contracts of SRW wheat, buyers of 1,000 corn, sellers of 6,000 soybeans, buyers of 1,000 soymeal, and sellers of 6,000 soyoil.

TENDERS

- CORN SALE: Leading South Korean animal feed maker Nonghyup Feed Inc. (NOFI) has bought an estimated 117,500 tonnes of animal feed corn in an international tender for up to 138,000 tonnes which closed on Wednesday.

- FEED WHEAT SALE: Leading South Korean animal feed maker Nonghyup Feed Inc. (NOFI) purchased about 80,000 tonnes of animal feed wheat expected to be sourced from Australia and other origins an international tender on Wednesday.

- FEED WHEAT SALE: South Korea’s Major Feedmill Group (MFG) purchased about 60,000 tonnes of animal feed wheat in a private deal on Wednesday without issuing an international tender,

- BARLEY SALE: Jordan’s state grain buyer has purchased about 50,000 tonnes of animal feed barley to be sourced from optional origins in an international tender which closed on Wednesday.

- RICE TENDER: South Korea’s state-backed Agro-Fisheries & Food Trade Corp has issued an international tender to purchase an estimated 79,439 tonnes of rice.

- FAILED CORN TENDER: Egypt’s state grains buyer GASC said it has canceled a corn purchase tender that closed on Wednesday with no purchase made.

PENDING TENDERS

- SOYBEAN TENDER: South Korea’s state-backed Agro-Fisheries & Food Trade Corp issued international tenders to purchase around 19,000 tonnes of food-quality soybeans free of genetically-modified organisms (GMOs).

- WHEAT TENDER: Jordan’s state grain buyer has issued an international tender to buy up to 120,000 tonnes of milling wheat which can be sourced from optional origins

- WHEAT TENDER: Egypt’s General Authority for Supply Commodities announced a tender for the purchase of wheat within the framework of the Food Security and Resilience Support Program funded by the World Bank under Loan No. EG -9399 with at sight financing. The deadline for offers is Feb. 2, GASC said.

US BASIS/CASH

- Basis bids for soybeans shipped by barge to the U.S. Gulf Coast were flat to lower on Wednesday on seasonally slowing export demand, while CIF corn basis bids were mostly steady to weak, traders said.

- Barge freight rates were mostly steady to lower as pressure from muted grain shipper demand was largely offset by reduced barge drafts at the Port of St. Louis and upriver, traders said. Low water prompted barge lines to restrict vessel drafts there, limiting the amount of grain that can be shipped in each barge.

- Export demand for U.S. Gulf soybeans has slowed as Brazil’s harvest is ramping following some rain delays. Chinese importers have been booking March and April shipments from Brazil this week, traders said.

- Bids for CIF soybean barges loaded in January were unquoted. February barge bids were 4 cents lower at 103 cents over March.

- FOB basis offers for February soybean shipments were steady at around 130 cents over March futures, while premiums for March shipments held at 120 cents over futures.

- Basis bids for CIF corn barges loaded in January were unquoted. February barges were bid a penny lower at 86 cents over March corn. March barges traded steady at 88 cents over futures before bids slipped to 87 cents over.

- FOB offers for February corn shipments held at around 90 cents over March, and March FOB offers were unchanged at 99 cents over futures.

- Spot basis bids for soybeans and corn were mixed at elevators around the U.S. Midwest on Wednesday, grain dealers said.

- Corn bids were steady to firm at processors, rising by 5 cents a bushel in Chicago.

- Processor bids for soybeans were unchanged.

- The cash basis for soft red winter wheat was strong, with the market underpinned by slow farmer sales in recent months.

- Farmer sales of all three commodities were slow on Wednesday.

- Grain dealers said that farmers had already priced enough deals to meet their short-term cash flow needs and were waiting to see if prices rally.

- Spot basis bids for soybeans were mixed at U.S. Midwest processors early on Wednesday, rising at plants west of the Mississippi River but falling at facilities in the eastern half of the region.

- Soy bids also were mixed at terminals along the region’s rivers.

- The soybean basis was weak at eastern elevators.

- Cash bids for corn were firm at river terminals and ethanol plants, and flat at interior elevators and processors.

- Farmer sales of both commodities were slow.

- Growers could afford to wait and see if prices rallied before committing to new deals, an Iowa dealer said.

- Spot basis bids for hard red winter wheat were unchanged at rail and truck market terminals across the southern U.S. Plains on Wednesday, grain dealers said.

- Farmers have been reluctant to sell old-crop supplies at current price levels, dealers said.

- Spot basis offers for U.S. soymeal held steady in both the rail and truck markets on Wednesday, dealers said.

- Supplies remained tight as low crush levels in recent months limited the amount of soymeal available for sale.

- Some processors were not posting offers and only delivering supplies to existing customers that had previously booked orders.

US Corn Used for Ethanol at 425.3M Bu in December

The following table is a summary of US corn consumption for fuel and other products, according to the USDA.

- Corn for ethanol was 11% lower than in December 2021

- DDGS production fell to 1.68m tons

US Soybean Crushings at 187M Bushels in December: USDA

USDA releases monthly oilseed report on website.

- Crushing 5.5% lower than same period last year

- Crude oil production 5.5% lower than same period last year

- Crude and once-refined oil stocks down 6.5% y/y

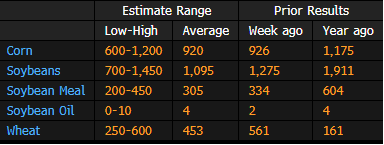

GRAIN EXPORT SURVEY: Corn, Soy, Wheat Sales Before USDA Report

Estimate ranges are based on a Bloomberg survey of six analysts; the USDA is scheduled to release its export sales report on Thursday for week ending Jan. 26.

- Corn est. range 600k – 1,200k tons, with avg of 920k

- Soybean est. range 700k – 1,450k tons, with avg of 1,095k

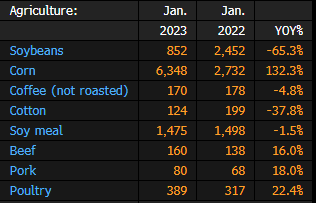

Brazil January Agriculture, Mining Exports by Volume: MDIC

Following is a summary of key Brazilian agriculture and mining exports by volume, from the Brazilian Trade Ministry.

- Corn exports rose 132% in January from a year ago

- Soybean exports fell 65% y/y

- Iron ore exports down 1% y/y

Brazil Soy Crop Revised Upward by StoneX on Early Harvest Signs

Higher yields in the majority of soybean areas that started harvesting compensate for a decline in estimated production from drought-stricken regions in Rio Grande do Sul, StoneX says in a report.

- Brazil soybean production estimated to reach 154.2m tons for 2022-23 season, up from 153.8m tons estimated in January

- Forecast for Rio Grande do Sul’s harvest was cut to 19m tons from 21.3m tons

- Yields are seen higher than previously expected in southeast, mid-east, north and northeast areas of the country

- Brazil’s summer corn crop estimate revised upward to 27.5m tons from 26.9m tons on higher yields in Minas Gerais state

- Rio Grande do Sul may reap 3.3m tons of corn, while initial forecasts called for 5.4m tons

- Brazil’s winter corn production is seen at 100.1m tons, above 99.6m tons in previous estimate

- Total corn crop may reach 129.9m tons, up from 123.5m tons in past season

Argentina Crop Exporters’ Sales Fell 61% y/y in January: Chamber

Argentina’s crop exporters sold $928 million in FX markets in January, 61% less than in the same month of 2022, Ciara-Cec, Argentina’s crop export and crushing chamber, said in a statement.

- Crop exporters also sold 75% less in January compared to the previous month

- The drop in sales last month was due to the effects of the drought in the agricultural sector and the early sales of soybean exports in December as a result of the FX measure known locally as “dolar soja” (soybean dollar), Ciara said

Argentine Soy Crop Seen at 36M Tons Amid Drought: USDA FAS

Soybean estimate is down 9.5m tons from the US Department of Agriculture’s official forecast for 45.5m tons after “dry weather and high temperatures in the last months of 2022” damaged plants, USDA’s Foreign Agriculture Service says in a report.

- Outlook is below 37m predicted by Rosario Board of Trade while Buenos Aires Grain Exchange said the crop could be as small as 35.5m

- NOTE: Argentina is the world’s third-biggest soy producer after Brazil and the US, and the country is the top shipper of soybean meal and soybean oil

EU Soft-Wheat Exports Rise 7.8% Y/y, Corn Imports Increase 73%

The EU’s soft-wheat exports in the season that began July 1 reached 18.8m tons as of Jan. 29, compared with 17.4m tons in a similar period a year earlier, the European Commission said on its website.

- Leading destinations include Morocco (2.76m tons), Algeria (2.5m tons), and Egypt (1.63m tons)

- EU barley exports were 3.12m tons, compared with 5.28m tons a year earlier

- Corn imports were 16.5m tons, against 9.49m tons a year earlier

- NOTE: The commission says some export figures for Germany may be inaccurate due to its recent shift to a new declaration system

- Also, Italian import data is only available until end-November

Top palm oil buyer India’s Jan imports fall to six-month low -dealers

India’s January palm oil imports fell 31% from a month ago to their lowest in months as a narrowing discount to rival oils prompted refiners to increase purchases of soybean and sunflower oils, five dealers told Reuters on Thursday.

The reduction in palm oil imports by India, the world’s biggest importer of vegetable oils, could weigh on Malaysian palm oil prices but support soyoil and help Russia and Ukraine in bringing down their sunoil stocks.

India’s palm oil imports fell to 770,000 tonnes last month, the lowest since July 2022, according to the average of the estimates from the five dealers with trading firms.

“Palm oil’s discount is coming down. Buyers are shifting to soyoil and sunflower oil,” said Sandeep Bajoria, chief executive of Sunvin Group, a vegetable oil brokerage and consultancy firm.

Palm oil’s discount to soyoil has shrunk to less than $300 per tonne from as high as $500 in the December quarter, the dealers said.

Palm oil’s share of India’s total vegetable oil imports has fallen as well, dropping below 50% in January from 71% in December, they said.

India’s soyoil imports in January rose 56% from a month earlier to 395,000 tonnes, while those of sunflower oil jumped 143% to a record 473,000 tonnes, the dealers said.

India raised sunoil imports as the oil has been trading at a discount to soyoil for the past few weeks amid efforts of top exporters Russia and Ukraine to reduce stockpiles, said a Mumbai-based dealer with a global trade house.

“Sunflower oil shipments rose to an extraordinary level. We never thought India could import this much sunoil in a month,” said a Singapore-based dealer.

India’s edible oil imports in the first quarter of the 2022/23 marketing year – which started on Nov. 1 – rose above 4.5 million tonnes while stockpiles at ports increased sharply, said a New-Delhi based dealer.

U.S. winter wheat production unchanged despite worsening drought across the Central Plains

2023/24 U.S. WINTER WHEAT PRODUCTION: 37.3 [34.1–40.5] MILLION TONS, UNCHANGED FROM LAST UPDATE

Outlooks for 2023/24 U.S. winter wheat planted area and production are unchanged at 36.1 million acres and 37.3 [34.1–40.5] million tons, respectively. As winter wheat remains dormant over the next few weeks, temperature and insulating snow cover are the key features to watch. While in the dormant stage, winter wheat typically is left unharmed with temperatures down to 0 °F, but becomes vulnerable to damage when temperatures reach and stay below -10 °F for a significant period of time (as it can kill the submerged growing point resulting in winterkill). If snow cover (above 1 inch or so) is present these cold temperatures might not be able to penetrate the snow’s insulating qualities. Winterkill is not a common occurrence in U.S. winter wheat production regions, as a combination of extreme low temperatures and little (less than 1 inch) or absent snow cover is a rare event.

In Winter Wheat and Canola Seedings (12 January), USDA set its initial estimate of 2022/23 plantings at 36.95 million acres, up 11% from last season. This prediction is directionally in line with what we have been calling for (first released on 14 September 2022), which suggested an upward shift in winter wheat plantings from last season’s 33.27 million acres. This season’s winter wheat yield potential is being greatly threatened by extreme drought conditions throughout the Plains, warranting close attention. The expanding drought across the Central Plains should be viewed as one of the biggest downside risks to the crop this season. The USDA’s latest monthly crop progress report (31 January) and many local reports continue to discuss the elevating risks of low soil moisture in some of the major HRW wheat regions. Kansas’ topsoil moisture supplies were rated 36% very short and 30% short, for example. Topsoil and subsoil moisture conditions in Oklahoma were rated mostly short, as nearly 90% of the state is currently in the moderate/exceptional drought category. Short-term forecasts indicate higher confidence for continued dry conditions next week, warranting attention. On the other hand, winterkill concerns remain low with warmer weather on its way and sufficient snow coverage present throughout the upper part of the Plains and the Midwest.

Brazil’s JBS says beef consumption to rise in China

Demand for beef in China is expected to rise as the country still has relatively low per capita consumption, Gilberto Tomazoni, chief executive of JBS SA JBSS3.SA, said on Wednesday during a business conference.

He said Brazil and the United States, where it has meat facilities, are well positioned to meet China’s growing demand for beef as the major food importer reopens after COVID-19 restrictions.

Farmers Pull Pack on Potash; Long-Term Contract Prices to Fall

Potash prices are poised to decline over the next six months as European buying fails to make up for disappointing North American demand. Green Markets expects the Chinese potash contract that ended in December to settle lower and later, at about $490 a metric ton, with growing downside risk. Chinese buying power is high, while North American suppliers are saddled with ample inventories. Global supplies have been building, particularly in the more liquid Western Hemisphere markets. Green Markets lowered its 2023-24 price forecasts while leaving 2025’s unchanged

The farmer pullback is global. Global imports are down 14% from a year earlier, with declines in the US (20%), Brazil (8%), EU-27 (35%) and India (17%).

Brazil Fertilizers Mixed Amid Reduced Need on Corn Crop

As nitrogen demand for safrinha winds down, ammonium sulfate and urea prices weakened in Brazil. Potash and phosphate prices remained stable amid an expected slowdown in soybean 2023/24 negotiations.

Nitrogen Weakens; Potash, Phosphates Stable: Wednesday Whisper

As safrinha off-season demand slows in Brazil, ammonium sulfate prices fell to $230-$240 a metric ton (mt) vs. last week’s $235-$250. Urea was also softening, though no clear price range emerged from the Fertilizer Latino Americano conference in Rio de Janeiro this week. Lack of demand for 2023-24 soybeans left potash prices unchanged at $500-$520/mt, though a bearish sentiment prevails as Belarus offers compete with Canadian and Russian sellers. MAP prices remained at $655-$660/mt amid tightening supply, while inland offers moved up $10-15/mt in Mato Grosso/Rondonópolis.

SOUTH AMERICA

UNITED STATES

This commentary is provided by ADM Investor Services, a futures brokerage firm and wholly owned subsidiary of ADM Company. ADMIS has provided expert market analysis and price risk management strategies to commercial, institutional and individual traders for more than 50 years. Please visit us at www.admis.com or contact us at sales@admis.com to learn more.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by Archer Daniels Midland Company. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS.

| CONFIDENTIALITY NOTICE

This message may contain confidential or privileged information, or information that is otherwise exempt from disclosure. If you are not the intended recipient, you should promptly delete it and should not disclose, copy or distribute it to others. |

Author

ADM Investor Services, Inc.