Corn futures post weak close after bullish reaction to Thursday’s report

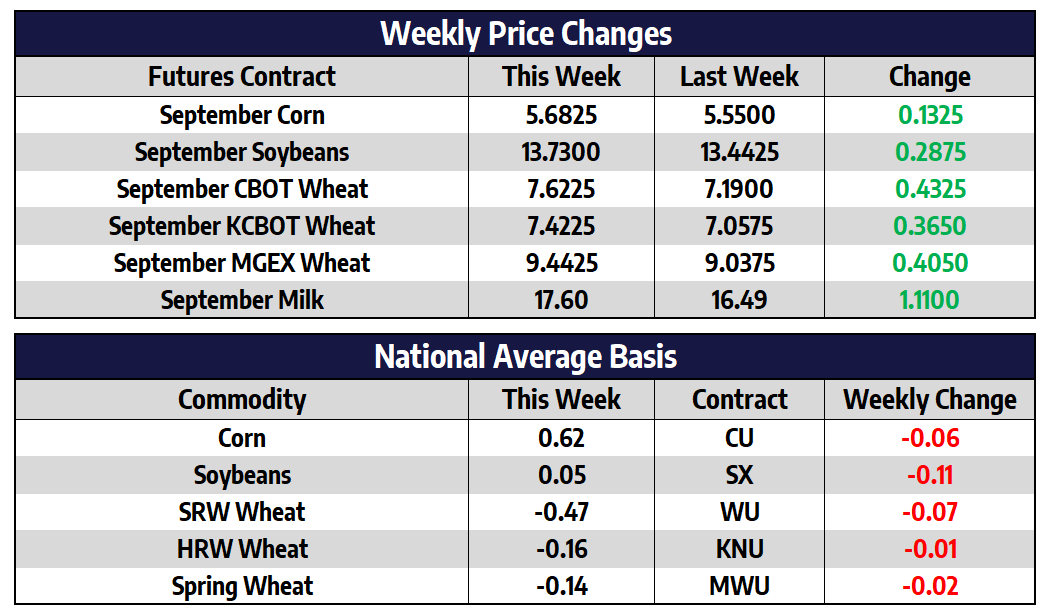

New crop December 2021 corn futures added 16-1/2 cents this week to close at 573. December of 2022 futures shed a 1/4 of a cent this week to close at 516. The average US corn yield for 2021 came in at 174.6 bushels per acre yesterday, this was down from 179.5 bushels per acre the USDA projected in July. The lower-than-expected yield number however included some projected record yields in the eastern Corn Belt. Illinois is slated for a record large corn crop averaging 214 bushels per acre according to yesterday’s USDA estimate. Indiana, Ohio, Michigan, and Pennsylvania are also expected to have record large crops. Very low yields are projected in the Dakotas and a 7-year low projected in Minnesota did the heavy lifting of dragging down the national average. This yield estimate was based on 18,630 farmer surveys as well as satellite data. Field surveys will be conducted over the next month to compile the September USDA yield estimate.

Using this new yield number, as well as an increased old crop carry in 2021/22, ending stocks are now estimated at 1.24 billion bushels, down from 1.43 billion projected in July. Feed usage and export demand were both lowered 100 million bushels for the 2021/22 marketing year. With a price action being rather weak into the market close on Friday, the trade will be paying close attention to next week’s open, as well as the Pro Farmer crop tour which will begin on Monday.

Soybeans higher this week after three weeks lower

New crop November 2021 soybean futures added 28-1/4 cents this week to close at 1365. November of 2022 futures shed 1-1/4 cents this week to close at 1256-3/4. Carryout levels for the 2021/22 soybean marketing year were unchanged from the July estimate on yesterday’s WASDE. While yield was slightly reduced from the July estimate, a larger old crop carry-in and a 20-million-bushel reduction to both crush and export demand left carryout unchanged at 155 million bushels. The new crop 2021/22 carryout has been at 155 million bushels for three months in a row now.

Much like the corn yield estimates the eastern belt is expected to have record soybean yields while the Dakotas and Minnesota are expected to see yields well below last year’s numbers. Illinois, Indiana, and Ohio are expected to have record state yields this year. Top soybean-producing state Illinois is estimated to have a record 64 bushel per acre crop this year. World ending stocks for soybeans came in at 96.15 million tons, 1.5 million tons larger than the trade was expecting. Both import demand and soybean crush demand in China were lowered by the USDA. Crush margins and hog profitability continue to struggle in the world’s top soybean importer, China. US cumulative soybean sales have reached 20.8% of the USDA forecast for the 2021/22 marketing year versus a five-year average of 20.2%.

All three wheat trade to contact highs on bullish report

September CBOT wheat futures added 43-1/4 cents this week to close at 762-1/4. September KC wheat futures added 36-1/2 cents this week to close at 742-1/4. September spring wheat futures added 28 cents this week to close at 944-1/4. US wheat production came in at a 19-year low on yesterday’s report. Reductions to Russia and Canada wheat crops also helped to support the wheat market this week. US 2021/22 all wheat production came in at 1.697 billion bushels, down from 1.746 billion in July. World wheat ending stocks came in at 279.06 million tons down from 291.68 million in July. September CBOT and KC wheat futures closed into new contract highs this week following the release of Thursday’s numbers.

Dairy Finishes the Week Strong

The dairy market has seen a choppy yet bullish week in terms of price action, as the Class III 2nd month contract finished $1.10/cwt higher than the previous week. Class III is the market taking the lead though, as Class IV has remained relatively stagnant on the week. The biggest catalyst to the higher price action for Class III has been in relation to higher cheese prices in the spot cheese market. To finish out the week, the spot cheese market finished out a whopping 15.875 cents higher. With the market closing at $1.63125/lb, the next technical upside objective is the July high of $1.70/lb. One potential factor that could push the cheese market substantially higher is the current spread between blocks and barrels. Barrels are substantially underpriced in comparison to blocks, and if they start to catch ground on blocks the market could rally quickly.

Going forward, we are still in the seasonal time frame that could support a slightly higher trend in prices. The fact that feed prices are remaining high after the release of the USDA’s WASDE report yesterday may start to pinch producers that are running out of feed contracts as we get into the awkward time frame between summer and harvest. Milk production has continued to stay strong over the last 6 months, but higher feed prices could help slow down this production growth. We won’t receive the next update from the USDA until August 22nd. Next week is a fairly quiet week with only the Global Dairy Trade auction showing up as a major update for the market.

Author

Keegan Madigan