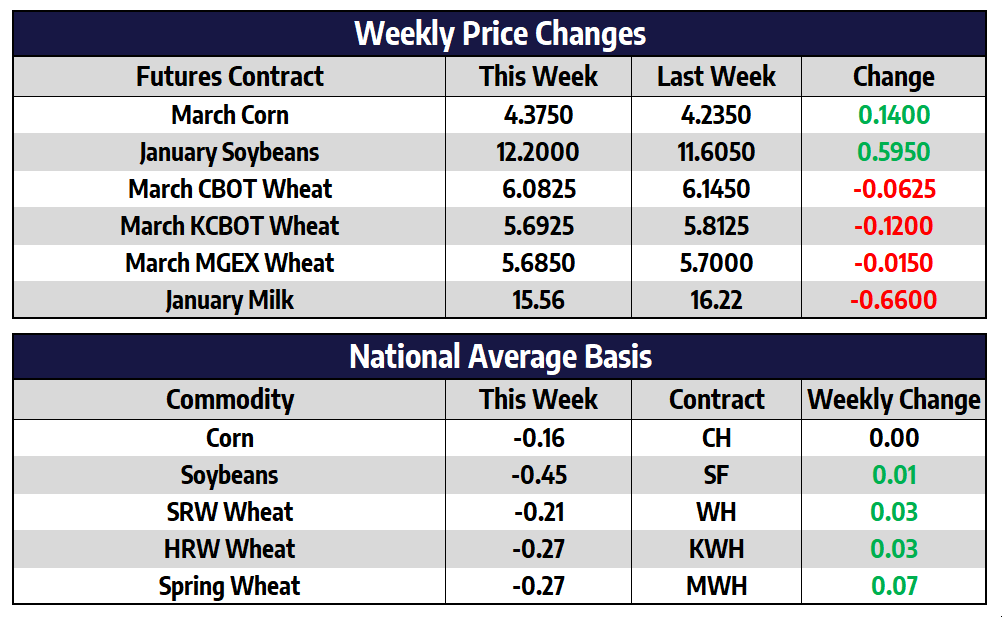

March corn futures rallied 14 cents this week to close into a new high of 437-1/2. December corn futures added 6-1/4 cents this week to close at 418-1/2. Marketing year corn export sales to date exceed the seasonal pace needed to hit the USDA’s record export target of 2.65 billion bushels by 259 million bushels this week. Actual corn shipments however fell short of the pace needed by 138 million bushels. US ethanol output dropped 3.4% week over week last week. This was the largest weekly drop since April. Ethanol stocks surged higher once again on a decline in usage. Stocks have rose 8% in the last two weeks, that is the second largest two-week rise since the pandemic began in March.The state of Mato Grosso is the largest corn producing state in Brazil and it is also Brazil’s largest corn exporting state. But, more of the state’s corn is now being consumed internally due to big increase in ethanol production. For the 2020/21 growing season, the Mato Grosso Institute of Agricultural Economics is forecasting a 2.3% increase in corn production. The institute is also forecasting a 18% increase to demand in the coming year due mainly to new corn-based ethanol facilities coming online and additional demand from the livestock producers. This is significant structural change for Brazil which at one time had more than 400 sugar mills that utilized sugarcane to produce sugar and ethanol. The increased internal demand across Brazil will leave less corn available for export in the coming year.

Front month January soybean futures found late week strength this week rallying 59-1/2 cents to close at 1220. November soybean futures joined the party rallying 28-1/2 cents this week to close into a new contract high of 1081-1/4. Forecasts call for rains across central and northeastern Brazil through the end of the year. Far southern Brazil and Argentina are expected to trend dryer than areas to the north in the coming weeks. As a whole these rains will be beneficial after a dry start to the growing season and especially now as South Americas soybeans begin to bloom and fill pods.

One of the main drivers of the soybean market this week was the continued sharp break lower in the US dollar. The dollar index broke below 90 index points this week to trade to a fresh 32-month low. Ongoing Coronavirus stimulus talks in Washington paired with an ever-expanding Federal Reserve balance sheet have slammed the US dollar lower since May. As a hedge against inflation physical assets such as gold and silver have pushed to multi year highs in the past few months. Historically a US dollar index below 90 index points has been supportive to physical assets and commodities as well as exports. The last extended stretch of the US dollar below 90 came between the years of 2005 and 2014 which was a rather friendly stretch for commodities.

Wheat slightly lower this week

March wheat futures were 6-1/4 cents lower this week to close at 608-1/4. March KC wheat futures lost 12 cents this week to close at 569-1/4. March Minneapolis spring wheat lost 1-1/2 cents this week to close at 568-1/2. Cumulative sales have reached 74% of the USDA forecast for the 2020/21 marketing year versus a 5-year average of 69.4%. Sales this week came in at 540,000 tons, this was near the upper end of the range of expectations. Sales need to average 183,000 tons per week to reach the USDA forecast. The US dollar fell to a new low and could continue to boost export interest in the short term. Uncertainty about Russian wheat exports and strength in other CBOT commodities should also be seen as supportive forces. March wheat should find support near the $6 area with first resistance coming in at this week’s high of 622.

Dairy Struggles, Ends The Week Red

The Class III milk market began the week with some promise as the spot markets were mostly bid higher on Monday and Tuesday followed by a Global Dairy Trade auction posting a 1.30% gain. Buyers were optimistic and even pushed some individual quarterly averages up to new all-time highs. Prices quickly reversed lower on Wednesday, though, from some profit taking, farmer selling, and perhaps because the market was getting a bit overbought. Thursday’s trade was sluggish as well, leading up to a milk production report that was expected to be bearish. The November milk production report did, in fact, show bearish increases in production, milk cows, and milk per cow which kept a weak tone in prices going into the weekend.

Market action on both Wednesday and Thursday this week show how quickly the market can change direction. It also showed how volatile this dairy trade continues to be. On Wednesday and Thursday, January 2021 class III milk fell a total of 68c while February 2021 dropped $1.18. It’s situations like this that we took into consideration when recently recommending OptionsPlus and Blended models get to 100% covered in Q1 2021 milk. Now that all milk is shored up through March (with stops in place to get to 100% covered in Q2 2021), it protects against the short term volatility of the market for the foreseeable future. Technically, the pullback in milk late this week still looks healthy after a strong run up in price. Next week’s trade will be important, though, as some support levels come back into play.

Author

Keegan Madigan