Corn continues to grind lower.

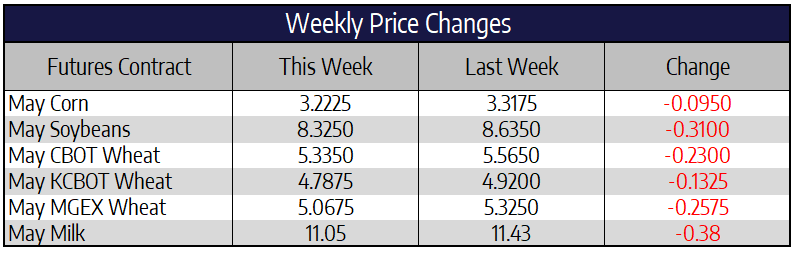

May corn futures traded down to contract lows this week, dipping 9-1/2 to close at 322-1/4. December futures also pushed to fresh contract lows this week, closing at 343-1/2, down 7-1/4 cents. Falling soil temperatures as well as a couple rounds of snow hindered any sort of corn planting progress across the heart of the Corn Belt this week. As we close in on the back half of April, with Mother Nature’s cooperation, a majority of corn planting will commence across much of the US.

The national corn index fell below three dollars a bushel this week. The last time the national average price for cash corn was this depressed was back in September of 2016. The biggest source of pain for the corn market remains the ethanol industry. Gasoline prices dipped to decades lows in a number of states this week. Extended stay at home orders point to continued reduced gasoline consumption in the coming weeks. Margins for ethanol plants seem to have stabilized around 25 cents negative per gallon produced. The main reason keeping margins from falling farther is the increased price in DDG’s as supply gets scarce. DDG prices have risen up over $200/ton in much of the corn belt, this compared with an average price per ton of $167 last month.

Soybean futures take a hit this week.

May soybean futures fell 31 cents this week to close at 832-1/2. November soybean futures were 24-3/4 cents lower this week closing at 851. According to Chinese customs data, China brought in 5.05 billion worth of US ag goods in the first three months of 2020. This would fulfill 14% of the phase one deal during the first quarter of 2020. Data also out of China this week showed their continued struggle to rebuild their hog herd from the impacts of ASF as well as COVID-19. Pork out put dropped to a 16-year low of 42.6 million tones in 2019. China slaughtered 131 million hogs over the first three months of 2020 down 30% from a year ago. The increase in feed demand to rebuild hog supply has pushed Chinese soybean futures to a 2 ½ year high.

After making their long trip across two oceans, Brazilian soybeans are now starting to arrive at southern China’s ports. Reports indicate the beans are being moved quickly to crush plants in China in attempt to rebuild soymeal stocks. Crush facilities have been idled in recent months, given the COVID pandemic as well as harvest delays in Brazil. With a flood of South American soybeans arriving at Chinese ports, the chances of China buying US beans in the near term, continues to dwindle.

Wheat follows corn and soy lower.

Chicago May wheat futures fell 23 cents this week to close at 533-1/2. May KC wheat futures fell just 13-1/4 cents this week, closing at 478-3/4. May Minneapolis Spring wheat was down 25-3/4 cents this week to close at 506-3/4. Better rain forecasts for the Black Sea region, mediocre US exports and US wheat missing sales to Egypt pressured futures this week. Old crop wheat export sales this week were rather light totaling 178,300 tons. Cumulative sales have reached 94.1% of the USDA forecast for 2019/20 vs the 5-year average of 96.2%. The marketing year for wheat wraps up at the end of May. Strong upside resistance on Chicago charts appears to be the 40-day moving average near the 5.36 mark.

Friday Finishes on a Quiet Note

Price action in the spot market on Friday was positive in every product other than non-fat powder. Whey has been the most impressive product this week, finishing up 4 cents on the week at $0.39/lb. Breaking over $0.40/lb has been a big obstacle for the whey market this year, and it would be impressive to see it trade over these levels. Cheese prices were up 0.5 cents in blocks and barrels today as prices consolidate just above $1.00/lb. This is the third lowest weekly close since 2000. Butter prices were the biggest winner on Friday gaining 2.75 cents to settle the week at $1.1875/lb.

The class III 2020 average was up $0.08 to $14.88 this week. Two weeks ago the 2020 average was settled at $14.83. While we have seen nearby contracts continue to weaken, more premium is being pushed back into the more deferred contracts. With the downturn in cheese the spread between Class III and Class IV has gone from $1.00 to $0.40 on the 2nd-month contracts.

Author

Lisa Heder