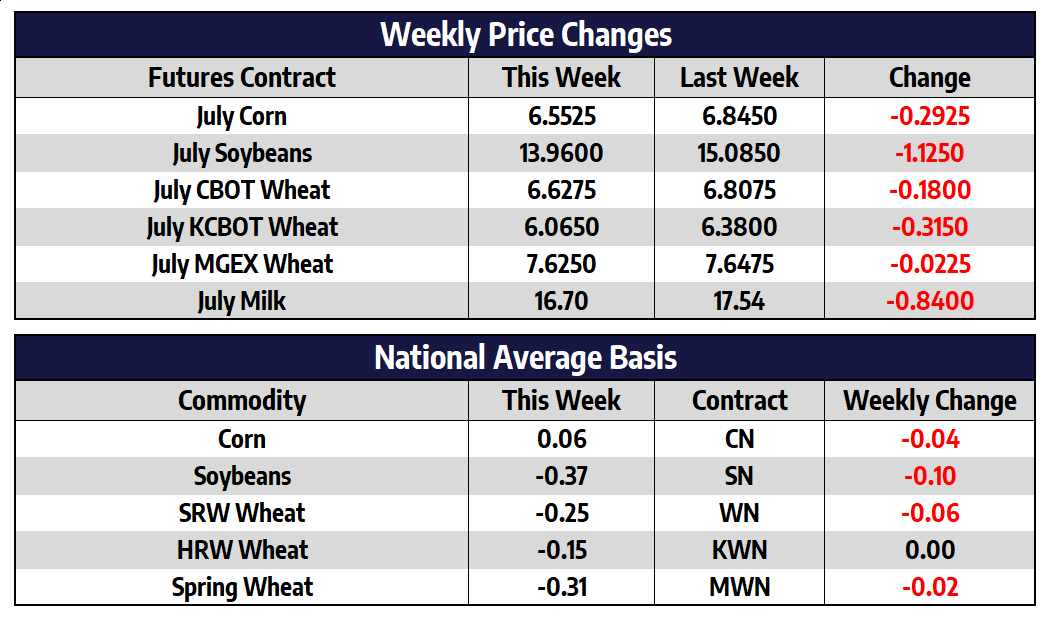

July corn futures shed 29-1/4 cents this week to close at 655-1/4. New crop December futures shed 43-1/2 cents this week to close at 566-1/4. December corn futures rallied 33 cents on Friday after falling the daily 40-cent limit on Thursday. Limits were expanded for Friday’s trade but will be back to the usual 40 cent limit for Monday. New crop prices were lower on the week and closed right at the 10-week moving average, a pivotal indicator in bigger bull markets. New crop prices have stayed above the 10-week average since November of 2020. Weather will continue to dominate headlines in the corn market over the next week and a half before the June 30th planted acreage and grain stocks report. This report is historically the most volatile report of the year for the corn market.

China announced this week it will grant 3.1 billion in subsidies to grain farmers, hopefully as soon as possible, to offset high fertilizer and diesel costs. This is all in an attempt to manage rising commodity prices by keeping farmers incentivized to produce big harvests this year. CFTC’s Commitments of Traders numbers which are normally released Friday’s at 2:30 CT will be delayed until Monday June 21st in observance of Juneteenth. The dataset will contain activity in the week ended June 15.

Beans fall sharply lower in wildly volatile week

July CBOT soybean futures shed 112-1/2 cents this week to close at 1396. November futures shed 125-3/4 cents this week to close at 1313. Weakness in global vegetable oils spilled over into the soybean market this week with beans falling over a dollar lower. Soybean oil along with other world edible oils have led the rally in soybeans over the last few months. Massive long liquidation hit the soybean complex along with the rest of the commodity sector on Thursday. Soybean prices opened sharply lower on Thursday morning and continued selling off sharply, closing more than 1.50 lower on front month beans. Prices managed to rally back somewhat on Friday, but weekly losses remained sharp.

Reuters reported Friday that China has bought at least eight cargoes of US soybeans out for the PNW for delivery in October. This comes after the historic drop in prices on Thursday, that total is around 18 million bushels. Rains this week disappointed in Iowa and southern Minnesota, but increasing chances over the weekend and into next week added market pressure. Cooler temperatures in the coming weeks are also expected to benefit the maturing crops.

Wheats lower this week as dollar rallies sharply

CBOT July wheat futures shed 18 cents this week to close at 662-3/4. July Kc futures shed 31-1/2 cents this week to close at 606-1/2. July MPLS futures shed 2-1/4 cents this week to close at 762-1/2. The US dollar rallied sharply higher this week, as the Federal Reverse announced sooner than expected interest rate increases. The dollar had its strongest week of 2021 this week, a stronger dollar makes US commodities less competitive in the world market. Given the sharp losses in corn and soybeans this week, wheat prices held up relatively well. Continued worry in Spring wheat production issues given the ongoing drought and heat in the northern plains helped support the other two wheats this week. The two winter wheats should continue to trend fairly closely with corn in the coming weeks. Harvest pressure in winter wheats could add pressure to the markets, however.

Dairy markets struggled this week, as every product on the CME’s spot trade was unable to finish higher on the week. The biggest loser of the week was the cheese market, as the block/barrel average dropped 6.875 cents. This drop lower was primarily driven by the barrel market, as barrels traded 13 cents lower this week. Last week we mentioned that the current spread between blocks and barrels could be a concern for the market, as barrels are very rarely at a large premium to blocks. This week we saw the spread unravel with barrels only holding a 5 cents premium over blocks vs. 17.25 cents a week ago. Whey, butter, and non-fat powder price all look similar recently with extended rallies earlier in the year now consolidating lower over the past few months. There is still the potential for these products to break out of their recent downtrend higher if global prices remain steeply higher than current domestic prices.

Futures markets continue to drag lower as spot markets hold steady or move lower. This week large drops in commodity prices across the board were impacting the milk market as well. Seasonals still hold that there could be a bounce at some point between now and July. Short-term indicators look oversold at the moment. That being said, a July to December average at $17.88 is still above average for the year a premium in the deferred contracts shows that the market believes there could be an additional upside to come in the spot markets at some point. The milk production report originally to be released today was delayed by the USDA in observance of Juneteenth.

Author

Keegan Madigan