Corn tumbles to end the week

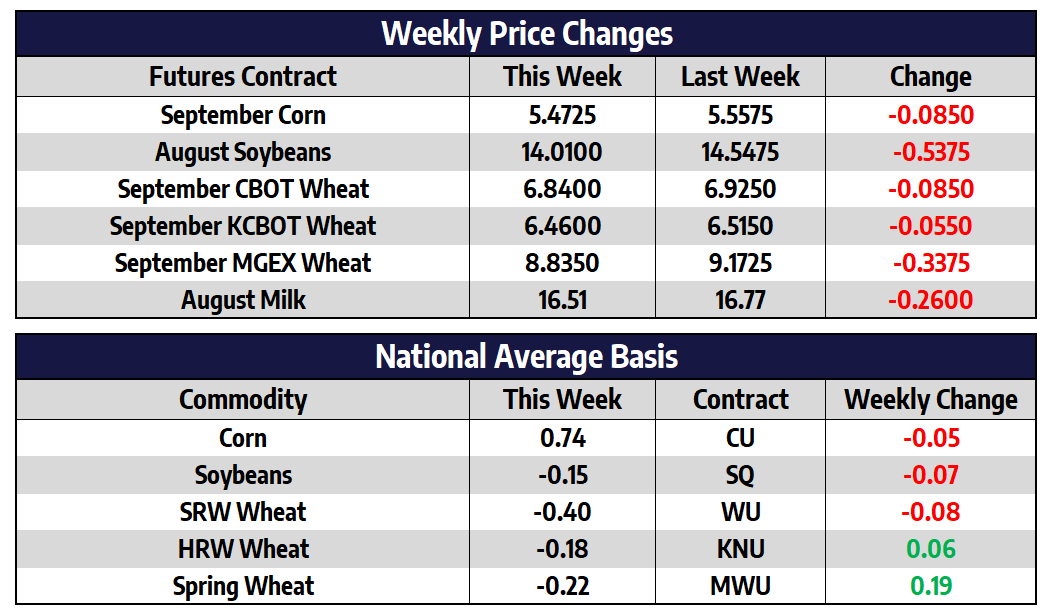

September corn futures fell 8-3/4 cents this week to close at 547-1/4. New crop December futures dropped 9 cents this week to close at 543. The US corn crop over ½ way through pollination as of Sunday, according to this weeks USDA crop progress report. New crop corn prices have not made a new high since early May and have also not made a new low since late May. While volatility has remained, prices have seemed content going nowhere fast trading between the 5 and 6 dollar per bushel levels the entire month of July. It has been eight weeks since China has purchased at least 100,000 tons of US new crop corn. Concerns are starting to arise among some traders as corn sales had begun to ramp up in a big way by early July last year.

US ethanol output last week topped one million barrels per day for the 10th consecutive week as reported in this week’s report. But stocks surged 6.5% to a five-month high implying the worst weekly ethanol usage since May 2020. Corn used in last week’s production is estimated at 103.9 million bushels. Corn use needs to average 97 million bushels per week to meet this crop year’s USDA estimate.

Soybeans fall to end the week

August soybean futures shed 53-3/4 cents this week to close at 1401. New crop November futures shed 40 cents this week to close at 1351-3/4. New crop soybean futures slid lower this week as weather model runs predicted cooler temperatures and increased precipitation in the coming weeks. August weather is historically the most important weather month for US soybeans, upcoming weather will be more closely watched than previous years as soybean supplies remain tight. Isolated storms are predicted for the Dakotas and Minnesota over the weekend and into early next week. While currently parched, even smaller rain amounts could go a long way in helping the Dakota’s soybean crop.

China’s soybean imports are expected to slow into late 2021 from a record first-half of the year according to a Reuters report this week. A key driver in the slowdown in soybean use in China has been the reversal in hog margins as new African Swine Fever outbreaks have sparked herd liquidations, surging output. Margins for hog producers are down more than 100% since the beginning of the year with a near-term turnaround no where in sight. China’s lack of interest in US soybeans as of late has some concerned the USDA demand projections may be overstated, China historically accounts for 60% of global soybean imports.

Wheat prices rally on tightening supply

September CBOT wheat futures shed 8-1/2 cents this week to close at 684. September KC wheat futures lost 5-1/2 cents this week to close at 646. September MPLS spring wheat futures shed 33-3/4 cents this week to close at 883-1/2. The US dollar neared its highest levels of 2021 this week against a basket of world currencies. Fear over global economic growth rather than a red-hot US economy have boosted the dollar in recent weeks. A surging US dollar makes US grains less competitive on the world market compared to other exporters. Falling corn prices late this week stymied any continued upside momentum in the wheat complex. The 100-day moving average comes in near the 670-mark on Chicago wheat. This should act as first support on a continued pullback.

Cheese Finds Stability to End the Week

The dairy trade has been dominated by the downturn in the spot cheese trade recently, as the market pressed into the lowest prices of 2021. After breaking into new lows, cheese buyers have come in to support the market back above what is seen as critical support of $1.48/lb. The market finished at $1.49375/lb, as the weekly close held support. Upside movement would look supportive that a short-term bottom may be in for the spot cheese market. Despite the spot cheese market trading to new lows, the futures market has remained relatively stable as the market seems to expect some seasonal strength to come into the market as we push through the summer.

Class IV prices have had low volatility this week as butter and non-fat powder made very minimal price movements on the week. The Class III vs. Class IV price spread has narrowed significantly in recent trade. Typically we would expect Class III to hold around $1.50 premium over the Class IV market vs. the current spread at 65 cents. This is something that may be supportive for higher Class III prices given the recent support the cheese market has seen.

Author

Keegan Madigan